The Housing Bubble and Financial Crisis as Central Planning by Government and the Promulgation of "Fake News" by Legacy Media - A Tale in Three Parts

PART I - President Clinton's Role in Creating the Housing Bubble - Precursor to Crisis

It is ironic that with the mainstream media in high dungeon over "fake news," that just a cursory review of some key events that led to the housing bubble and financial crisis will reveal legacy media as the chief purveyor of "fake news." In particular, the government's enormous role in causing the housing bubble has gone almost completely unreported. When the topic of government's role in causing the crisis has come up, the media - which has a Pavlovian predisposition to bigger government - has routinely attempted to squash this notion. This reflexive desire to protect the government's reputation - and to suppress what should be any journalist's deep-seated suspicion of those in positions of great power - will be demonstrated by using the example of the New York Times' Paul Krugman.

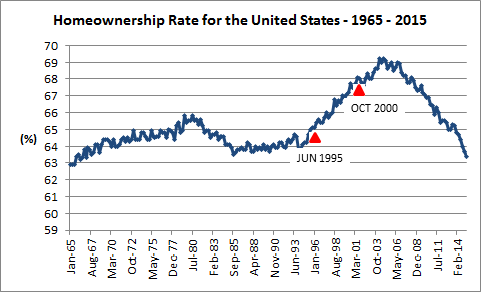

The cursory review here of the decade or so prior to the collapse of Lehman Brothers in 2008 will show the critical role the government played in creating the financial crisis. While any number of speeches or pieces of legislation can be used to demonstrate this critical role, perhaps the best is a June 5, 1995 speech by President Bill Clinton. (1) In this speech President Clinton elaborated on what he called his homeownership strategy - read central plan. In an act of economic hubris and ignorance co-equal with that of any Soviet-era commissar, Clinton announced a specific homeownership goal - to three significant digits no less - for the entire US, 67.5%. This goal was well in excess of historic levels of homeownership and had no basis in any sort of rigorous economic analysis. Indeed, the best evidence is that the 67.5% goal was merely plucked from thin air. See the Chart below, data from the St. Louis Fed (2);

For the remainder of his term in office, President Clinton along with his two housing secretaries - Henry Cisneros and Andrew Cuomo - would move heaven and earth to achieve the 67.5% homeownership goal. The "success" of their efforts can be seen in the rapid - albeit temporary - increase in homeownership rates starting just prior to 1995. The significance of October 2000 - which corresponds to the supreme and terminal act of economic idiocy associated with Clinton's homeownership central plan - will be described in Part II. All that needs to be understood now is President Clinton's central plan for housing - like nearly all the central planning goals of the Soviet Union - could be achieved. However, the achievement would fundamentally alter the make-up of the nation's economy and create enormous economic hardships. Moreover, the longer the government perpetuated economic house of cards continued to exist, the greater the resulting economic damage that would be sustained when it inevitably collapsed.

President Clinton and his housing secretaries would seek to advance their homeownership goals through three primary conduits. Two of these conduits were legislation that provided the executive branch enormous influence over the housing market. The other conduit used the government's ultimate and greatest power - what the great Murray Rothbard likened to the "velvet glove on the mailed fist." (3)

- The affordable housing (AH) mandate of the ironically entitled Federal Housing Enterprises Financial Safety and Soundness Act.

- "Best Practices Agreements" between banks and HUD (the velvet glove on the mailed fist)

- "Reforms" to the Carter-era Community Reinvestment Act (CRA)

Each of these conduits and the manner in which they enabled the Clinton administration to goose housing markets will be briefly described.

Because of its contribution to the housing bubble and enormous losses suffered by the government sponsored enterprises, (GSEs), Fannie Mae and Freddie Mac, the best description of the Federal Housing Enterprises Financial Safety and Soundness Act is Orwellian. The act had two primary provisions. First - and in a sop to the many members of Congress eager to have mortgage money flow more freely - the act required Fannie and Freddie to establish specific goals for the percentage of GSE mortgages that went to low and moderate income borrowers. In 1993 - and prior to the Clinton administration unleashing chaos on the housing market - only about 34% of Fannie mortgages when to low and moderate income borrowers, while the percentage for Freddie was about 30%. (4) By the end of the Clinton presidency these percentages were well on their way to soaring past 50%.

The second provision of the act - and a sop to those members of congress concerned about even more government influence in the housing market - required the establishment of an office to oversee Fannie and Freddie. This office was the Office of Federal Housing Enterprises Oversight (OFHEO). OFHEO had the unenviable task of taking on two of the most politically connected organizations in Washington - Fannie and Freddie. For as long as anyone could remember, all sorts of well-connected administration "officials" and Washington insiders had landed in very profitable perches at Fannie and Freddie. Indeed, just before it was forced to re-state billions of dollars in completely fictitious profits, the chair and vice-chair of Fannie Mae were Franklin Raines and Jaimie Gorelick. Raines was Clinton's former budget director, and Gorelick was Clinton's former deputy attorney general. These two individuals - and their four Harvard degrees - had no experience in the mortgage industry and were completely unqualified to run what would become the world's largest home mortgage company. Nevertheless, Raines and Gorelick were both paid tens of millions of dollars to ultimately cause tens of billions in losses.

The affordable housing mandate allowed the government to exert a tremendous amount of influence in the housing market via the GSEs, but the large mortgage banks were untouched by the affordable housing mandate. In order to have the large mortgage banks lend in a manner to support Clinton's homeownership goal, starting in September 1994 HUD Secretary Cisneros negotiated "best practices" agreements with the private mortgage banks. In essence, these agreements required the private mortgage banks to adopt many of the same policies as the GSE's, and to lend more freely than the banks had in the past. The first of these agreements was signed with the nation's largest mortgage bank, Countrywide Financial. There is evidence to suggest that the government used some arm-twisting to get the mortgage banks to sign these agreements. Many people - including members of the financial crisis inquiry commission - believed the "best practices" agreements were signed under what can be considered duress, namely the threat of pulling the mortgage banks "under the umbrella of the CRA." (5) This was the government exerting its power through the "velvet glove on the mailed fist."

The reformed CRA also imposed significant changes to the mortgage market. Chief among these changes was the reformed CRA emboldened a host of "public advocacy groups" that were also seeking to expand homeownership. These groups - the largest and most infamous of which was the Association of Community Organizations for Reform Now (ACORN) - used the public comment process that preceded bank mergers or acquisition activities to protest numerous banks on CRA grounds. These protests were notorious for their fury and routinely garnered large - and largely favorable - media attention. Groups like ACORN then used threats of these CRA-fuelled protests to essentially extract further concessions from lenders to loan more freely.

With the affordable housing mandates, the "best practices" agreements with mortgage banks and a reformed CRA inspiring zealots at ACORN and elsewhere, everything was in place for the government to advance its homeownership goals - the consequences be damned.

Peter Schmidt

August 26, 2018

ENDNOTES

1. Remarks on the National Homeownership Strategy by President William J. Clinton, June 5, 1995, http://www.presidency.ucsb.edu/ws/index.php?pid=51448

2. Economic Research Federal Reserve Bank of St.Louis, Homeownership Rate for the United States (RHORUSQ156N) https://fred.stlouisfed.org/series/RHORUSQ156N

3. Murray Rothbard, America's Great Depression, Ludwig von Mises Institute, Auburn,AL 2000, p. 188

4. U.S. Housing Market Conditions Summary: HUD Prepares to Set New Housing Goals, Table 1, https://www.huduser.gov/periodicals/ushmc/summer98/summary-2.html

5. Phil Angelides and Bill Thomas, The Financial Crisis Inquiry Report, p. 523