A Safe, Flexible & Stable Monetary and Financial System: The Fed Provides This?

INTRODUCTION:

Believe it or not, this is what the Fed thinks of itself;

"The Federal Reserve, the central bank of the United States, provides the nation with a safe, flexible and stable monetary and financial system." (1)

A review of the Fed's own data will show that, far from providing safety, flexibility, and stability, the Fed is a progenitor of financial chaos and wealth concentration.

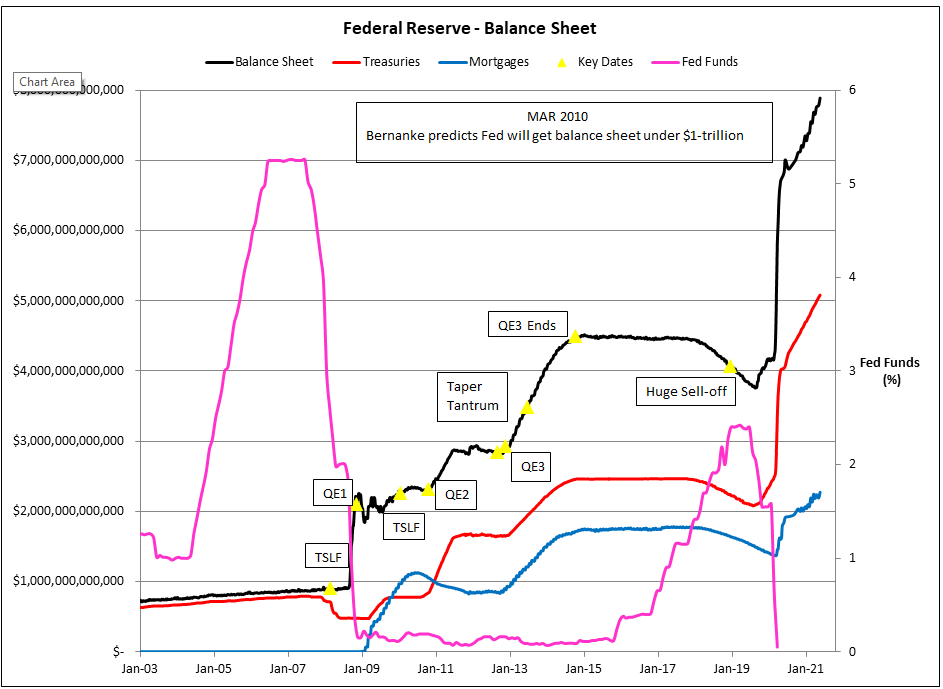

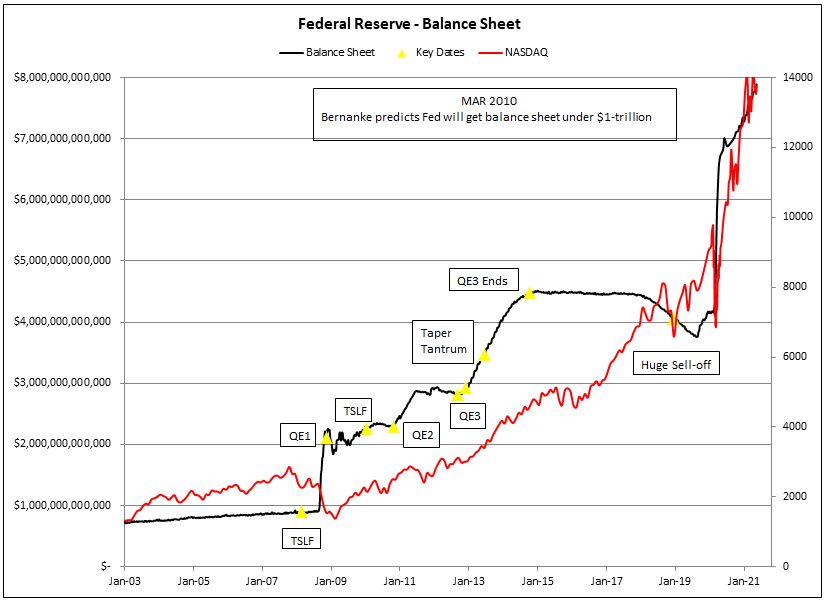

In the charts below, the Fed's balance sheet is plotted along with the portions comprised of government debt, (Treasury securities), and mortgages, (mortgage securities). Also plotted are the Fed funds rate, (Figure 1) and the Nasdaq average, (Figure 2). The Figures also reference a handful of the Fed's post-2008 programs, including the various rounds of quantitative easing, (QE), and the the Term Securities Lending Facility (TSLF). In the TSLF - which was the Fed's first post-2008 emergency intervention program - the Fed traded Treasuries for debt securities. Once QE was underway - where the Fed conjured trillions of dollars out of thin air and used this magical money to purchase toxic assets from the firms that helped cause the crisis - the TSLF program was redundant.

As part of reviewing this data, it is useful to keep the following assessments from several senior Fed officials in mind. By doing so it will become clear that, far from proceeding along a well-ordered and completely understood path, the Fed's post-crisis interventions are haphazard stop-gaps, and the Fed has no understanding of how the economy will respond to any of its programs. The assessments to be reviewed are not cherry-picked. Rather they come from the officials - Ben Bernanke, James Bullard and Janet Yellen - who dominated the policy discussions and subsequent implementation.

- 25 MAR 2010: Ben Bernanke promises to get the balance sheet under $1-trillion. (2)

- June 2010: James Bullard of the St. Louis Fed describes the Fed's QE programs as "temporary in nature" and "always meant to be temporary in nature." (See #3, p. 156)

- 01 JUN 2014: St. Louis Fed, "The FOMC has stipulated that the expansion of the Fed balance sheet is temporary (emphasis in the original) and that holdings will return to normal as the recovery progresses." (4)

- 14 JUN 2017: Janet Yellen cavalierly dismisses any concerns with the Fed reducing its balance sheet and compares the process to "watching paint dry." (5)

SUMMARY of OBSERVATIONS:

- Twice in the past 20-years, interest rates have hovered at just over 0%. Prior to this recent history, rates this low were unheard of. (Figure 1)

- Prior to 2008, the Fed never owned a single mortgage security. Now, nearly thirteen years after the housing bubble burst, the Fed owns over $2-trillion of them, and continues to buy more each day. (Figure 1)

- Home prices have blown past their housing bubble peak, and yet the Fed continues to purchase mortgage securities. (Figure 1)

- Many people credit the Fed for 'saving' the economy after 2008. However, this judgement is premature. The Fed's operation can only be considered complete when the Fed returns its balance sheet to the levels it had in September 2008. The Fed is headed in the opposite direction. (Figure 1)

- Whatever your opinion on QE, QE3 was inexcusable. The Fed double-downed on this mistake when they folded in the face of the Fed's 'taper tantrum.' (Figure 2)

- At the time of the taper tantrum, the Nasdaq was ~4000. Eight years later the Nasdaq would advance 250%. Now that stocks have risen so much because of the Fed's monetary tailwinds, the Fed is trapped by its own profligacy. It can't reign in the money supply without crashing the stock market house of cards it built. (Figure 2)

- Proof of this is Janet Yellen's confident prediction that the Fed cutting its balance sheet 'would be like watching paint dry.' However, in December 2018 - when the Fed was cutting its balance sheet - stocks cried uncle and collapsed. The Fed would have none of this and was soon increasing the money supply, months before the Covid crisis. (Figure 2)

- The economic calamity produced by the Covid inspired 'lockdowns' wreaked enormous havoc. It is not hyperbole to describe the ensuing economic contraction as "the worst since the Depression." Yet in that disastrous economic contraction what did the Nasdaq do? It rose almost 75%! Figure 2.

FIGURE 1

FIGURE 2:

CLOSING REMARK:

For the past several weeks, numerous Fed officials have said the Fed has the 'tools' to deal with inflation. Presumably these tools include cutting its balance sheet and raising rates. Based on the data contained in Figures 1 and 2, any confidence in the Fed to cut its balance sheet or raised rates in unjustified..

Peter Schmidt

Sugar Land, TX

June 06, 2021

PS - As always, if you like what you read, please register with the site. It just takes an e-mail address and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book. Registering with the site will give you access to the entire Confederacy of Dunces list as well as the financial crisis timeline.

Help spread the word to anyone you know who might be interested in the site or my Twitter account. I can be found on Twitter @The92ers

ENDNOTES:

1. This link also contains the balance sheet data used to compile Figures 1-3.

https://www.federalreserve.gov/releases/h41/

2. See the video, starting around the 1:04 mark;

https://www.youtube.com/watch?v=v4He1m2a5jg

3. James Bullard, "The Lessons for Monetary Policy from the Panic of 2008," Federal Reserve Bank of St. Louis Review, May/June 2010, pp. 155-163

https://files.stlouisfed.org/files/htdocs/publications/review/10/05/Bullard.pdf

4. Christoper J. Waller and Lowell J. Ricketts, "The Rise and (Eventual) Fall of the Fed's Balance Sheet," Federal Reserve Bank of St. Louis, January 1, 2014

https://www.stlouisfed.org/publications/regional-economist/january-2014/the-rise-and-eventual-fall-in-the-feds-balance-sheet

5. Yellen said, "My hope and expectation is that when we decide to go forward with this plan, (reducing the balance sheet), there will be very little reaction to it, that's how we intend to proceed, and that this is something that will just run quietly in the background over a number of years, leading to a reduction in the size of our balance sheet and in the outstanding stock of reserves, and this is something that the Committee will not be reconsidering from time to time. We think this is a workable plan, and it will as one of my colleagues, President Harker described it, it will be like watching paint dry." See page 17 of the link. https://www.federalreserve.gov/mediacenter/files/FOMCpresconf20170614.pdf