Chickens Coming Home to Roost - Alan Greenspan and Charlie Sheen Chaperone the Junior Prom

William McChesney Martin chaired the Federal Reserve from 1951 - 1970, and remains the longest serving Fed chair. Martin famously described the job of the Fed, or any central bank for that matter, as being no different from a chaperone who "takes away the punch bowl just as the party starts to really get going." The idea is a central bank should lean against the wind and help to check the growth of any speculative excess or manias. Because this job description still implicitly accepts the notion of an "active" central bank complete with central planners masquerading as central bankers, it is hardly completely accurate. Nevertheless, the notion of a central bank providing a settling, sobering influence on markets and the economy has considerable merit. If we use Martin's sobering influence as a standard of central bank efficacy, then the Federal Reserve of the Alan Greenspan era can be likened to Hollywood playboy and ne'er do-well Charlie Sheen chaperoning the junior prom through the streets of Amsterdam.

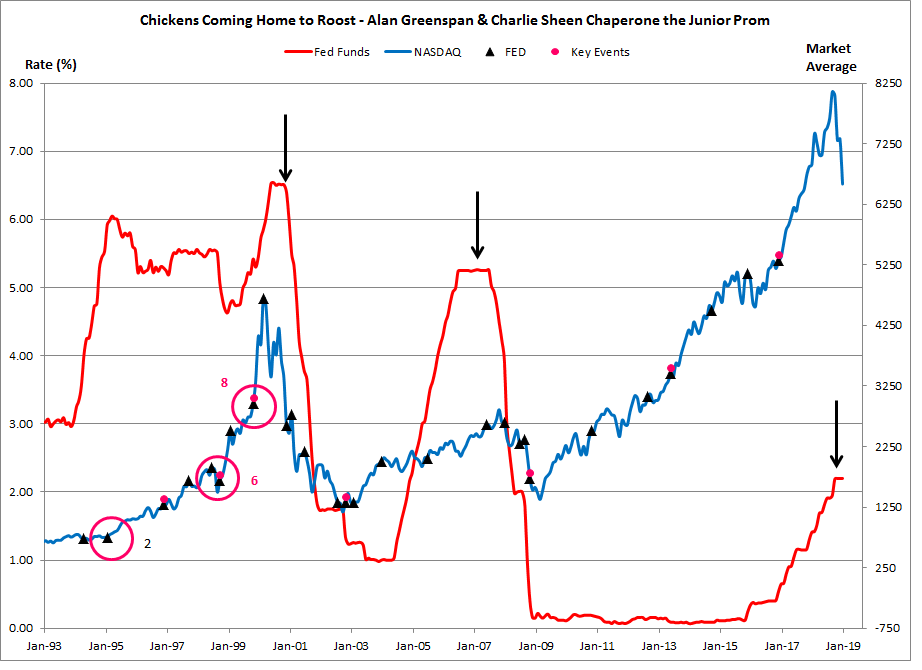

The above chart was first introduced in a previous blog post. (1) However, rather than listing all 28 Fed "events" that led up to today's precarious market position, only three are shown. These three events - all of which relate to the enormous contribution the Greenspan Fed made to the speculative mania that characterized the tech bubble era - are as follows;

- Event #2 - Greenspan & Robert Rubin bailout Mexican bondholders (FEB 95)

- Event #6 - the "most irresponsible act" in Fed history, the extraordinary rate cut following LTCM's collapse (OCT 98)

- Event #8 - portions of the Glass-Steagall Act are repealed (the "Citigroup Relief Act) (NOV 99)

First, each of these events will be described. Second - and most importantly - these three events will be discussed as a collective whole in the context of everything that came after them, today's market turmoil in particular.

Greenspan & Robert Rubin Bailout Mexican Bondholders (#2)

The so-called "Tequila Crisis" shows us two things.

- Banking isn't nearly as complicated as most bankers would have us believe.

- There really isn't anything new under the financial crisis sun.

The Tequila Crisis refers to the crisis that developed around Mexican bonds in late 1994 and early 1995. Like many countries, when the Mexican government borrows money from outside Mexico it must borrow in foreign currencies, typically the US dollar. However, the Mexican government collects its tax revenue in pesos. If the peso falls in value against the dollar - and it has done this many times in the past - it will take far more pesos to pay back the same debt denominated in dollars. This "currency risk" is part and parcel of the risk associated with lending money to any country that borrows in one currency and obtains revenue in another currency. Over the years, this simple, immutable fact has been the source of one "international debt crisis" after another.

However, at the time of the Tequila Crisis the banks that would have been left holding the bag if Mexico defaulted had an ace in the hole - Alan Greenspan. For some reason that only Alan Greenspan can fathom, he decided to intervene on behalf of Mexican creditors when the peso suffered a precipitous fall in late 1994. There wasn't an enormous amount of money at stake - perhaps $50-billion in total - and the stability of world banking system would not have been impacted in the slightest if all that money had died and went to money heaven. Greenspan worked with Treasury Secretary Robert Rubin, (Dunce #41), to craft an aid package that President Clinton,(Dunce #12), subsequently turned into the Mexican Stabilization Act. Congress - correctly - balked at this and rejected what was rightly criticized as a transparent attempt to bail out the banks who lent money to Mexico.

One of the banks that would have almost certainly been left holding the bag if the Mexicans defaulted was Goldman Sachs. As the ex-CEO of Goldman Sachs, Treasury Secretary Rubin wasn't going to let that happen. Of course, in any sort of honest government, Rubin would have recused himself from playing any role in any plan that would provide enormous benefit to his former employer. Transparency in government aside, Rubin then used the Exchange Stabilization Fund, (ESF), (2) to buy pesos on the open market which stabilized the peso. Additional loan guarantees were provided and the Mexican government was eventually able to make good on its debts.

While some people - even today - see the actions of the Fed and the Treasury Department in a positive light, the interference in the functioning of credit markets during the Tequila Crisis numbed creditors to the enormous - and obvious - risks associated with international lending. As a result of the failure to appreciate these enormous and obvious risks, when the next international lending crisis came - which it did as the 1997 Asian currency crisis - it proved to be far bigger than the crisis which was supposedly averted in Mexico in 1995.

The "Most Irresponsible Act" in Fed History (#6)

In the Tequila Crisis, Alan Greenspan's attempt at providing succor to the world's biggest banks was greatly assisted by Robert Rubin, ostensibly Treasury Secretary of the United States but really little more than Goldman Sachs' errand boy. In the LTCM crisis, Greenspan didn't need any help at all and is thus solely responsible for all the enormous problems resulting from the aftermath of the LTCM crisis.

Long-Term Capital Management (LTCM) was a collection of MIT PhDs who thought they could become fantastically wealthy by picking up pennies in front of runaway freight trains. (3) Oscar Wilde famously defined a cynic as someone who knows the cost of everything and the value of nothing. LTCM duplicated the behavior of Wilde's cynic by employing statistical correlations of past price action to predict prices in the future. LTCM applied all sorts of complicated mathematical and statistical analysis to this historical data, and used this analysis to identify what it thought prices should be in the present. If the actual price was different than the price that LTCM thought it should be, then LTCM would make "bets" with other market participants about whether the current price would move to the priced predicted by LTCM or not. These "bets" - and that is what they were - were made with"derivatives." (See the Lawrence Summers dunce biography, (#45), for more on derivatives.)

There were many logical problems with LTCM's entire business model, not the least of which was that it confused correlation with causation. However, on the investment level the biggest problem was leverage. Because the difference between actual prices and the prices predicted by LTCM's models was typically quite small, the only way for LTCM to make serious money was to use enormous amounts of leverage. It was not unusual for LTCM to borrow $30 for every $1 of its own capital. Because LTCM poured all its winnings into future investments, LTCM was always one bad trade away from a complete collapse, and that is why their entire business model can be likened to picking up pennies in front of runaway freight trains. LTCMs complete collapse came in September 1998. (See the Jon Corzine dunce biography, (#13) for a description of how Goldman Sachs took advantage of LTCM's collapse.)

LTCM was a small hedge fund headquartered in Greenwich, CT. It had perhaps a few hundred employees. However, Greenspan and the entire Fed apparatus was greatly concerned about LTCM's collapse. On September 23, 1998, the NY Fed organized a bailout of LTCM to ensure that LTCM's collapse didn't spawn a wave of panic selling. During the next scheduled meeting of the Fed's Open Market Committee (FOMC), September 29, Alan Greenspan cut interest rates to help dampen the sell-off in stocks that LTCM's collapse seemed to inspire. (This dip is visible in the chart above.) However, even all this wasn't enough for Alan Greenspan. On October 15, 1998, Alan Greenspan cut interest rates again - this time between regularly scheduled meetings of the FOMC. Investment professional Bill Fleckenstein correctly calls this "one of the most irresponsible acts in Fed history."

The Citigroup Relief Act (#8)

The Citigroup episode provides another example of the Greenspan Fed's enormous role in the formation of enormous asset bubbles - the ramifications of which the economy is still dealing with. As with the examples provided by the Tequila and LTCM crises, the Citigroup episode provides another example of the Greenspan Fed's willingness to serve as Wall Street's indefatigable lackey.

In April 1998, Citicorp and Travelers Insurance announced their decision to merge under the name Citigroup. Travelers was a large insurance company that also controlled Salomon Brothers, a large securities firm. On the other hand, Citicorp was the largest bank holding company in the US. Combining these two entities would put investment banking and commercial banking activities under a single corporate structure - something specifically prohibited by the depression-era Glass-Steagall Act. How could financial services veterans such as Sanford "Sandy" Weil (Travelers, Dunce #48) and John Reed (Citicorp) make such a blunder, and propose a merger that was surely prohibited by existing legislation and thus "illegal"?

As it turned out, it wasn't an blunder at all. Weil and Reed knew the proverbial fix was in. Before announcing the merger, Reed and Weill had met with President Clinton, Treasury Secretary Rubin and Greenspan to obtain their endorsement of the merger. All three officials endorsed the merger. (4) Their endorsement of the merger made the subsequent passage of the Gramm-Leach-Bliley Act in November 1999 a fait accompli. (Gramm refers to Phil Gramm, Dunce #28) The Glass-Steagall act was a piece of legislation, and the Greenspan Fed had no real standing to discuss whether such a long-standing law needed to be changed or not, particularly when a large, powerful corporation stood to benefit so much from this law being changed.

Indeed, on Wall Street the Gramm-Leach-Bliley Act was more accurately termed the "Citigroup Relief Act." This characterization, and the animating thought process behind it, does much to demonstrate that by November 1999 Wall Street became even more convinced that they had a tremendous ally in Alan Greenspan. Greenspan's intervention in the Citigroup affair - along with his previous bailout of LTCM and the subsequent "emergency" rate cut of October 1998 - directly coincide with a speculative boom on Wall Street. See the chart above and the highlighted items #6 and #8.

In October 1998 - at the time of Greenspan's emergency rate cut, (#6), the NASDAQ stood at 1611. By November 1999 and the passage of the "Citigroup Relief Act," (#8), the NASDAQ had risen to 2967, a gain of 84% in thirteen-months! From November 1999 to the NASDAQ's March 2000 peak of just over 5,000, the NASDAQ rose another 70%, this time in just four months! The animals spirits - which McChesney Martin believed a central bank should help subdue and moderate- were obviously being encouraged and emboldened by the Greenpan Fed. To use McChesney Martin's anology of a central bank serving as a sobering kill-joy, Greenspan was chaperoning the party exactly like Charlie Sheen would. What better evidence of this is there than in the above chart which shows an enormous climax run corresponding to Greenspan's active intervention in the market?

Concluding Remarks:

Alan Greenspan and the Greenspan Fed have much to answer for in the generation of the tech bubble. As discussed here, rather than being a sobering influence on the market, they encouraged market excess. They did so by shielding Wall Street from losses (Mexico, LTCM) and encouraging Wall Street's fascination with the "bigger is better" mindset of corporate structure (Citigroup). While this brief discussion establishes the huge role Alan Greenspan and his Fed played in the formation of the tech bubble, what does this have to be with the subsequent financial crisis of 2008 or today's market turmoil?

As shown in the chart, after the tech bubble collapsed, Alan Greenspan slashed interest rates. Mortgage rates fell in sympathy with Greenspan's enormous rate cuts. With lower mortgage rates, the same mortgage payment could be used to purchase more expensive homes. These low - and constantly lower - interest rates then provided the rocket fuel that shot housing prices higher and higher. Coupled with the lending profligacy encouraged by the Clinton White House, (5), and its 67.5% "goal" of homeownership, the housing market exploded. Homeownership peaked at just over 69% in April 2004, and the Federal Funds rate at the time was just 1%. With hardly any homebuyers left and rates already at historic lows, an enormous financial house of cards had been created. The slightest perturbation would send the entire structure crashing to the ground.

Of course, when the financial house of cards that had been built up around the housing market collapsed, the Fed intervened again, and embarked on even greater involvement in the economy - most especially through its asset purchases and quantitative easing (QE) programs. These interventions - like the previous Fed interventions in advance of the tech and housing bubbles - sent the prices of all sorts of assets soaring. The first round of QE is shown as Item 22 in the chart, and the NASDAQ began its enormous run to 8000 soon after. However, as with the tech and housing bubbles, a completely unstable financial structure has apparently been created. Indeed, many people feel that today's "everything bubble" dwarfs the combined excesses of the tech and housing bubbles. Regardless of its size or the ensuing impacts from any subsequent collapse, today's everything bubble was actually authored decades ago by Alan Greenspan as part of his efforts to blow up the tech bubble. Few people in the financial news media appreciate the long-running nature of today's volatile markets.

Peter Schmidt

13 JAN 2019

PS - As always if you like what you read, please consider registering with the site. It just takes an e-mail address, and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book! Registering with the site will give you access to the entire Confederacy of Dunces list as well as the Financial Crisis timeline. Both of these are a treasure trove of information on the crisis and the long-running problems that led to it.

ENDNOTES:

(1) Chickens Coming Home to Roost - the Fed and Twenty-Five Years of Price Suppression, http://www.the92ers.com/blog/chickens-coming-home-roost-fed-and-25-years-price-suppression

(2) The ESF goes back to the FDR administration of the 1930s and FDR's confiscation of privately held gold. FDR confiscated all privately held gold and paid its former owners $20.67 for each ounce of gold confiscated. However, immediately after collecting all this gold, FDR then devalued the dollar from $20.67 per ounce of gold to $35 per ounce of gold - a 70% devaluation! This enormous windfall to the government provided the basis for the ESF, and the ESF remains under the complete control of the Treasury Department. Henry Paulson tapped into the ESF during the 2008 crisis as well.

(3) Here is a sample of the educational and professional background of several LTCM partners, all of whom eventually became infamous when LTCM crashed; Greg Hawkins (BS and PhD, MIT), Larry Hillibrand (PhD MIT), William Krasker (PhD MIT, Harvard Professor), Robert Merton (PhD MIT, MIT and Harvard Professor, Nobel Laureate in Economics), David Mullins (BS Yale, PhD MIT, Harvard Professor, Vice-Chair Federal Reserve), Eric Rosenfield (BS and PhD MIT), Myron Scholes (MIT and Stanford Professor, Nobel Laureate in Economics).

(4) Arthur E. Wilmarth, Jr. "The Road to Repeal of the Glass-Steagall Act," Wake Forest Journal of Business and Intellectual Property Law, Volume 17, Summer 2017, Number 4, pp. 513-515, https://scholarship.law.gwu.edu/cgi/viewcontent.cgi?article=2556&context=faculty_publications

(5) See the recent blog post which details Andrew Cuomo's role in the generation of the financial crisis and the personification of the lending profligacy required to achieve President Clinton's goal of 67.5% homeownership. http://www.the92ers.com/blog/andrew-cuomo-halloween-far-more-terrifying-michael-myers