A Day Which Will Live in Financial Infamy - October 15, 1998

"One of the most irresponsible actions in Fed history."

William Fleckenstein and Frederick Sheehan on the emergency rate cut of October 15, 1998 (1)

The 23rd anniversary of the Greenspan Fed's emergency rate cut on October 15, 1998 went unnoticed by markets and the financial media. This is remarkable because this emergency rate cut laid the basis for everything that came after it; namely the generation of an enormous bubble in tech stocks, an even larger housing bubble and finally a still larger "everything" bubble. (Note: the designation of the rate cut as 'emergency' is the result of the rate cut occurring between regularly scheduled meetings of the Fed's Open Market Committee, FOMC.)

The precipitating cause of the Greenspan Fed cutting rates between scheduled FOMC meetings was the collapse of the hedge fund Long Term Capital Management (LTCM). LTCM seemed to have more MIT PhDs working for it than MIT. Basically, what the MIT educated geniuses of LTCM thought they could do is utilize computers to make a fortune by picking up pennies in front of runaway freight trains. LTCM gathered all sorts of statistics around prices and used this data to predict what prices should be. Anytime the market price differed from the computer predicted price, LTCM would make – by using highly complicated, highly leveraged financial derivatives – what were essentially bets or wagers that the market price would move to the price predicted by the computer. Because the spreads or difference between the prices predicted by the computer and the prices prevailing in the market were often very small, the only way to make serious money using this strategy was to use enormous leverage. Some idea of the leverage LTCM used can be gleaned by understanding that it was not unusual for LTCM to have $30 of borrowed money invested for each $1 of its own capital invested. With this amount of leverage, a trading loss of approximately 3% results in insolvency.

LTCM was comprised of perhaps no more than a few dozen employees working in a relatively small office in Greenwich, CT. However, LTCM’s financial footprint would become enormous and - if the Fed is to be believed – so large that LTCMs failure would threaten the functioning of financial markets all over the world. After a few years of enormous success, LTCM began to suffer enormous losses. Because of its early successes, LTCM had been able to borrow huge amounts of money. As it teetered on the brink of solvency in September 1998, it was estimated that LTCM may have had as much as $1-trillion in market exposure through its various derivative trades. As is the Fed’s want to do, the Fed organized a bailout of LTCM.

The failure of LTCM – which was acknowledged to have some of the smartest people in finance working for it - offered the real prospect of finally instilling some much-needed and long overdue discipline on Wall Street. The failure of LTCM could have been similar to a person swearing off even having a single drink before driving as a result of a near-miss accident while drinking drunk. However, and not unlike some overly indulgent uncle spoiling his favorite ne’er-do-well nephew even as the boy’s parents try to instill some sense of discipline and responsibility, Uncle Al intervened to save all his favorite nephews on Wall Street.

After cutting interest rates on September 29, 1998 – the first scheduled meeting of the FOMC after the LTCM bailout – Greenspan called a special meeting of the FOMC on October 15. At this meeting, Greenspan wanted to cut interest rates again. Apparently, Uncle Al didn’t think organizing the LTCM bailout and cutting rates once was enough support for Wall Street. Greenspan was trying to mobilize the FOMC to get behind him to provide still more succor and support for Wall Street. Greenspan did have some resistance on the FOMC, most notably from Don Poole. Poole trenchantly asked, “Is there any chance the action today (cutting rates) could be viewed by some anyway as an effort to bail out the hedge funds?”

As it turned out, it was a 100% certainty that the October rate cut would be viewed as an effort to bail out hedge funds. Speculators all over Wall Street became convinced that no matter how recklessly they acted, there was a limit to how bad things would get. If things started to even look like they might become bad, then Uncle Al and the Fed would bail them out. This mindset became known as the “Greenspan put.”

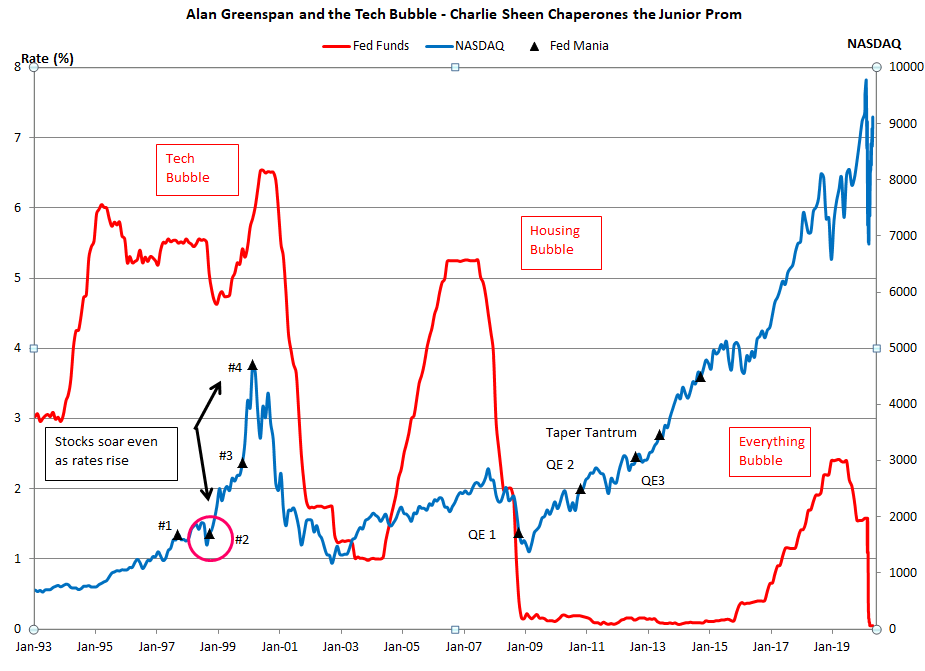

In investing a put allows a security to be sold for a certain price and basically limits the loss from an investment. The “Greenspan put” was a financial backstop for all of Wall Street and, not surprisingly, Wall Street acted completely recklessly as a result. In the case of the October 1998 rate cut between scheduled FOMC meetings, a manic sense of “irrational exuberance” clearly engulfed Wall Street. At the time of the surprise rate cut the NASDAQ was at 1611. In a little over a year, November 1999, the NASDAQ soared to 2967, a gain of 84%. In a final speculative blow-of the NASDAQ reached 5000 in March of 2000, a 70% rise in just the four months since November, or over 210% since the surprise rate cut sixteen-months earlier in October 1998. See Figure 1. Note that Item #2 is the emergency rate cut of October 15, while Item #3 indicates the passage of the 'Citigroup Relief Act,' (the partial repeal of Glass-Steagall).

FIGURE 1:

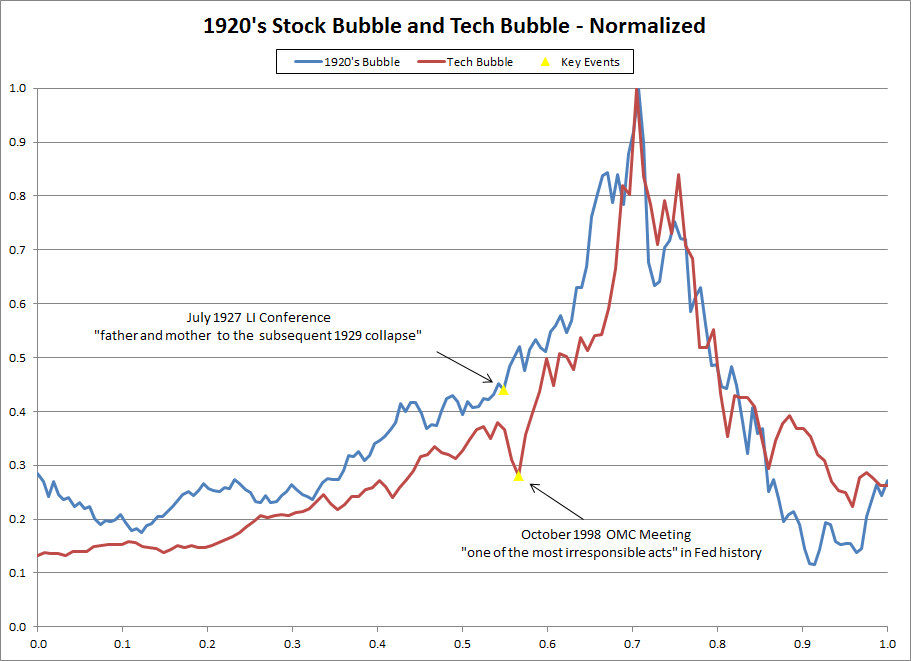

The stock market climax following the October 1998 surprise rate cut was a case of history repeating itself, and eerily similar to the stock market blow-off that followed the July 1927 Long Island conference of central bankers. The July 1927 meeting of central bankers was called by Ben Strong, governor of the Federal Reserve Bank of New York. The goal of the meeting was to coordinate a policy of loose money or interest rates cuts among the central banks of the US, France and Germany. The policy of loose money had one purpose – to advance the economic interests of England. While France and Germany balked at the policy, Strong pursued it with vigor. Adolph Miller of the Federal Reserve and a contemporary of Benjamin Strong’s, called the credit expansion decided upon at this meeting and implemented by Strong afterwards the “father and mother to the subsequent 1929 collapse.”

Figure 2 chart plots the 1920’s stock bubble for the period January 1920 – September 1933 and the tech bubble for the time period from January 1993 – March 2003. The data in the chart is “normalized.” Normalization is a technique commonly used in statistics when evaluating data measured over different durations of time that is also measured using different scales of magnitude. As Figure 2 makes clear, the 1920s stock bubble and the tech bubble of the late 1990s share many similarities, not the least of which is they were both sparked by the unique combination of arrogance and stupidity that can only be found among central banks and PhD economists.

FIGURE 2:

In the 1920s, the criminal irresponsibility of the Federal Reserve and Ben Strong led to an enormous stock bubble, the collapse of which helped to cause the Great Depression. In the 1990s, the criminal irresponsibility of the Federal Reserve and Alan Greenspan led to an enormous stock bubble, the collapse of which led the Fed to slash interest rates. This dramatic drop in interest rates then fueled the terminal stages of the housing bubble. When the housing bubble burst, the United States then suffered its largest economic setback since the Great Depression. This setback then prompted a series of unprecedented policy responses by the Fed which fueled an asset bubble larger than the tech and housing bubbles put together. This entire chain of events started with the actions of a single day - 15 OCT 1998!

Peter Schmidt

October 17, 2021

Sugar Land, TX

PS - As always, if you like what you read, please consider registering with the site. It just takes an e-mail address, and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book! Registering with the site will also give you access to the entire Confederacy of Dunces list as well as the Financial Crisis timeline. Both of these documents are a treasure trove of information on the crisis and the long-running problems that led to it.

ENDNOTES:

1. William Fleckenstein and Frederick Sheehan, Greenspan's Bubbles - The Age of Ignorance at the Federal Reserve, McGraw-Hill, New York, 2008, p. 51