Derivatives and the Financial Crisis - An Introduction to the Timeline

The timeline is an enormously large and complex document. Here, the content related to the role derivatives played in the crisis has been distilled and presented in a relatively compact manner. Full citations, including links to the source documents, are available in the download of the timeline.

Summary:

- Derivatives had been a topic of concern among the banking industry as far back as 1992.

- A Lehman insider discussed the risks his firm was exposing itself to in May 1998.

- The CFTC proposed regulating derivatives in May 1998; LTCM collapsed in September 1998.

- The Clinton Administration and the Fed led the July 1998 fight against regulation.

- Even after derivatives played an enormous role in the collapse of LTCM, Rubin, Summers, Greenspan and others did not change their opinion on regulation.

- The Fed's rate cuts after LTCM's collapse fueled a massive stock market bubble.

- The net capital rule was changed, and this allowed much greater amounts of leverage.

- The change to the net capital rule was a consequence of a over-reliance on "models."

- AIG's derivative trade in mortgage bond "insurance" also relied heavily on models.

- Well before Lehman's collapse, there was much discussion about mortgage derivatives.

- Until just before the financial crisis peaked, Henry Paulson at the Treasury and the NY Fed's Tim Geithner were clueless about what was happening on Wall Street.

- Geithner negotiated the Fed's bailout of AIG and folded in the face of Wall Street.

- The majority of the AIG bailout, $60-billion, went to AIG's derivative counterparties.

January - September 1992 – Financial Community Warned About the Dangers of Derivatives

In a speech to the New York Bankers Association Gerald Corrigan, the Governor of the Federal Reserve Bank of New York, cautions about the danger of financial derivatives. He warns bankers that they need to “take a very hard look at off balance sheet activities (derivatives)” and “I hope this sounds like a warning because it is.” Later that year Allan Taylor, Chairman of the Royal Bank of Canada, likened derivatives to a “time bomb that could explode just like the LDC crisis did, threatening the world financial system. (The LDC crisis was the crisis spawned by hundreds of billions of debt to third world countries going bad.) Picking up on the bomb metaphor, Felix Rohatyn, a senior partner at investment bank Lazard Freres, envisioned the market for derivatives as “26-year olds with computers creating financial hydrogen bombs.”(1)

May 1998 – Lehman Executive Makes the Mistake of Telling the Truth, Pays the Price

John Succo was an executive with the investment bank Lehman Brothers and a personal friend of James Grant of Grant’s Interest Rate Observer. Succo agreed to speak at a symposium organized by Grant’s because he was growing increasingly concerned about the enormous leverage that was increasingly being seen in derivatives trades all over Wall Street. Of particular concern to Succo was the ease with which hedge funds like LTCM were able to enter trades with leverage often in excess of 100:1 (2) At the symposium, Succo committed the unpardonable Wall Street sin of telling the truth. In particular, he described how Lehman’s senior management was nearly completely ignorant of the risks Lehman was exposed to in their derivative contracts;

“I don’t think that the people running our firm, our equity floor, have any idea of the things that we actually do, of how we…(audience laughter)…I’m serious…of how we hedge, the products that we’re involved with, the amount of risk we take or the lack of risk we actually take.” He also says of Lehman’s management, “…if your making money, (management) kind of leaves you alone until there is a crisis situation. And I don’t think that’s a way to run a firm.” (3)

Comment: After hearing a tape of the speech, Lehman fires Succo.

May 7, 1998 – CFTC Proposes Regulating Derivatives

Commodities Futures Trading Commission and its commissioner, Brooksley Born, float the idea of regulating over the counter derivatives.

July 30, 1998 - Clinton and Fed Officials Argue Against Regulating Derivatives

Assistant Treasury Secretary Summers - who would later become president of Harvard - testifies to Congress that derivatives do not need to be regulated. Summers was joined in opposing Brooksley Born's proposal by, among others, Alan Greenspan and Robert Rubin.

August 1998 - Street-smart Trader Outsmarts MIT PhDs

Vincent Mattone - a former trader at Bear Stearns and a personal friend of Long Term Capital Management's (LTCM) founding partner John Meriwether - visits LTCM's Greenwich, CT headquarters. LTCM, after years of success, has started to suffer enormous losses. Mattone asks Meriwether how much capital LTCM has lost. When told by Meriwether LTCM has lost 50% of its capital in the past few weeks, Mattone quickly - and correctly concludes - "Your finished. When you're down by half-people figure you can go down all the way. They're going to push the market against you." (4)

Comment - Unlike the MIT PhDs and Harvard professors - whose ridiculous ideas formed the basis for LTCM's trading strategies - Mattone recognizes that markets are human affairs, not scientific exercises.

September 21, 1998 - LTCM Suffers Enormous Losses While Goldman Profits

LTCM loses $533-million in a single day, more than it had lost in the previous month. The losses equal one-third of LTCM's capital and basically made their situation hopeless. Traders believe that Goldman - which has access to LTCM's trading book - is taking advantage of this knowledge and "banging the s--t out" of LTCM's trades from the start of trading in Japan. This day seals LTCM's fate.

September 23, 1998 - Fed Bails Out LTCM but Refuses to Revisit Derivatives

The Fed organizes a consortium to purchase LTCM in spite of a competing offer that required no Fed involvement. In spite of the leading role derivatives of the type Brooksley Born was so concerned about playing such a major role in the collapse of LTCM, Alan Greenspan, Robert Rubin and Lawrence Summers do not reconsider their position on the wisdom of regulating these trades.

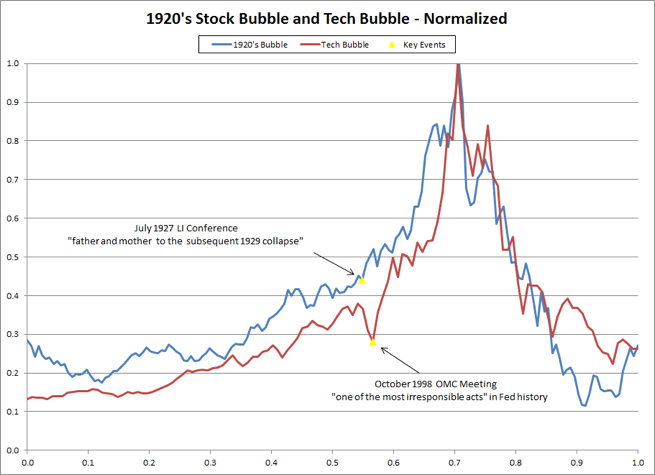

October 15, 1998 – One of the Most Irresponsible Acts in Fed History (Greenspan Put)

Acting between regularly scheduled meetings of the FOMC, the Greenspan Fed cuts interest rates again. Bill Fleckenstein calls the Fed cutting rates to 4.75% between scheduled meetings in the immediate aftermath of the LTCM collapse - “one of the most irresponsible acts in the history of the Federal Reserve.” (6) From this point until the market crash in March 2000, stocks will soar. In fact, the stock market performance will prove eerily similar to another stock market boom – this one in the late 1920’s – fueled by another bout of Fed incompetence, the 1927 meeting of central bankers.

February 15, 1999 – Time Praises the Economic Knowledge of Three Economic Charlatans

Time magazine features Alan Greenspan, Robert Rubin and Lawrence Summers on its cover with the title, “The Committee to Save the World.” The financial crisis will expose these men as consummate frauds and financial charlatans.

November 12, 1999 – Portions of the Glass-Steagall Act Removed

President Clinton signs the Gramm-Leach-Bliley Act which removes provisions of the Glass-Steagall Act that placed limits on the relationship a bank could have with a securities firm. The act passed the House 343-86 and the Senate 90-8.

February 29, 2000 – Goldman’s Henry Paulson Argues for More Leverage on Wall Street

“In addition, we and other global firms have, for many years, urged the SEC to reform its net capital rule to allow for more efficient use of capital. This is the single most important factor in driving significant parts of our business offshore…”(7) The change to the net capital rule will allow much greater amounts of leverage to be used by Goldman, Bear Stearns, Lehman, Merrill Lynch and Morgan Stanley.

April 28, 2004 – Net Capital Rule Changed, Firms can Use Much More Leverage

In 2004 and as a result of industry “urgings” from the likes of Henry Paulson and others, the net capital rule was changed. In its place, the SEC decided to allow the largest Wall Street firms, the broker-dealers, to use “an alternative risk-based approach to satisfy the Commission’s regulatory capital requirements, instead of using the current net capital rule.” (8) The SEC’s tolerance for much higher levels of leverage seemed to be based in large part on supposedly more accurate and more sophisticated computer models.

End of 2005 – Deutsche Bank Trader Warns AIG of Risks in its Credit Default Business

Greg Lippmann of Deutsche Bank flies to London to meet with AIG Financial Products, the biggest insurer of sub-prime mortgages and the long-side of his short bet against mortgages he owned via the credit default swaps. Lippmann tries to convince AIG to stop selling insurance on credit default swaps. (9)

August 16, 2006 – Paulson Admits to Ignorance of Derivatives Market

“…I explained how on Wall Street, if you had a big inventory of bonds, you could hedge yourself by buying credit derivatives, which were relatively new instruments designed to pay out should the bonds they insured default or be downgraded by a rating agency…Credit derivatives, credit default swaps in particular, had increasingly alarmed me over the past couple of years…No one knew how much insurance was written on any credit in this private, over-the-counter market.” (10)

September 08, 2006 – Jim Grant Predicts Massive Losses on ‘Trillions’ in Mortgages

“Overvalued, we, in fact, judge trillions of dollars of asset-backed securities and collateralized debt obligations to be, and we are bearish on them. …housing related debt is cheap by no standard of value. For institutional investors equipped to deal in credit default swaps, there’s an opportunity to lay down a low-cost bearish bet.” (11)

"He (a CDS buyer) looks for “high Florida exposure, high California exposure, high second-lien exposure. You look for equity take out loans because those appraisals tend to be overstated, a high percentage of stated-income loans (a.k.a. liars’ loans) and you build yourself a portfolio of credits from weak underwriters that are ultimately likely to be impaired.” (12)

Comment: This is the playbook investors will use to purchase "insurance" on mortgage bonds from AIG. The financial "models" that AIG relies on are riddled with enormous holes and gaps.

September 22, 2006 –Grant’s Interest Rate Observer Discusses Mortgage Market Excess

“…the issuance of complex mortgage structures is booming when house prices are not and the visible and looming difficulties in residential real estate have not yet depressed the prices of such instruments as…CDOs… Everyone is playing the same game, which is: As long as the problems don’t occur too soon, we are all okay.” (13)

September 28, 2006 – Merrill Lynch Correctly Predicts Massive Losses in Mortgage Bonds

Merrill Lynch in its Review of ABS Markets predicts that with as little as 5% depreciation in house prices losses in mortgage backed bonds will eat into even the triple-A rated tranches.” (14)

October 6, 2006 – Grant’s Interest Rate Observer Predicts Huge Losses in Mortgages

“At last report 44% (of sub-prime mortgages) were characterized by limited documentation, 31% by piggyback loans and 22% by interest only…The article goes on to conclude that a drop in housing prices of only 4-7% will completely wipe out even the AAA tranche of a mortgage backed collateralized debt obligation.” (15)

Fall 2006 – Deutsche Bank Trader Details Coming Mortgage Collapse to Hundreds of Investors

Greg Lippmann of Deutsche Bank had made his case for shorting mortgage securities to as many as 250 large investors privately and to hundreds more at Deutsche Bank sales conferences. (16)

Early July 2007 – “Dude, You Owe us $1.2-billion”

As a result of losses in the sub-prime market the “insurance” on the bonds backed by sub-prime mortgages became increasingly valuable. Deutsche Bank has purchased some of this insurance, via credit default swaps, from Morgan Stanley. Deutsche Bank’s Greg Lippmann calls Morgan Stanley’s Howie Hubler and states, “Dude, you owe us 1.2-billion.” (17)

August 2007 – Goldman Sachs Demands Collateral From AIG for its Winning CDS “Bets”

Goldman Sachs demands $1.5 billion in collateral from AIG as a result of a drop in the value of mortgage backed securities that AIG provided “insurance” on. (18)

August 9, 2007 – Paulson Finally Awakens to the Financial Firestorm Already Under Way

Paulson cites this day as the day the ‘crisis in the financial markets that I had anticipated arrived in force and it came from an area he wasn’t expecting, housing. The specific problem was BNP Paribas, France’s largest bank, had halted redemptions from funds holding mortgage bonds. The European Central Bank (ECB) ultimately announces that 49-banks borrowed $130-billion, more than they did in the aftermath of the 9/11terrorist attacks. (19)

December 2007 – AIG Executives Citing the Work of a Wharton Professor Dismiss Concerns

Martin Sullivan, AIG CEO, addresses investor’s concerns about the company’s credit default swap exposure by stating that Prof. Gary Gorton’s models give AIG “a high level of comfort”. Gorton explains that no transaction is approved if it is not first based on the computer model. Joseph Cassano, head of AIG’s financial products unit, credits Gary Gorton of Wharton with helping to develop the “intuition” that the financial products division used to build their business. He also says the models the financial products unit uses are “simple, they’re specific and they’re highly conservative. (20) The trades being discussed here will generate over $60-billion in losses.

December 05, 2007 – Wharton Professor Extols the Virtues of the Models He Provided to AIG

Gary Gorton on the models he put together for AIG to use in pricing their credit default swaps, the “models are guided by a few, very basic principles, which are designed to make them very robust and to introduce as little model risk as possible. We always build our own models. Nothing in our business is based on buying a model or using a publicly available model.” (21)

February 28, 2008 – AIG Announces Enormous Losses on its Credit Default Swaps

AIG announces an unrealized $11.5-billion loss on its credit default swaps.

May 8, 2008 – AIG Admits to Even More Losses in Mortgages

AIG announces additional $9-billion in unrealized losses to its credit default swap portfolio bringing the total to over $20-billion.

September 11, 2008 – Geithner Notes Lehman Needs $230-billion in Short-Term Funding

Tim Geithner briefs Treasury department officials on the investment bank Lehman Brothers. Geithner nonchalantly claims that Lehman needs to secure $230-billion in “overnight” repurchase agreements or “repos” to keep its business going. (22)

September 13, 2008 – Paulson Admits to Ignorance of Problems at AIG

During meetings in an attempt to save Lehman Brothers Chris Flowers of Bank of America asks Paulson if he knows how bad things are at AIG. Paulson would admit in On the Brink, that he knew AIG was having trouble but he didn't expect this.

September 16, 2008 – Unelected Fed Officials Implement $85-billion Bailout of AIG

“We have 800 billion.” At 9:00-pm the Federal Reserve announces an $85-billion loan to AIG and assumes a 79.9% equity stake in the company. (23)

Week of November 03, 2008 – Geithner Takes Over AIG Negotiations, Folds Like Origami

NY Fed President Tim Geithner takes over negotiations on behalf of AIG in their effort to negotiate terms with creditors on the value of their credit default swaps. Because of AIG’s financial position AIG was proposing “haircuts” or reductions from “par” (full) value of the underlying CDS contracts. (24) Geithner will cave to all the creditor’s demands even though in bankruptcy proceedings creditors are often forced to settle for pennies on the dollar.

November 05, 2008 – Paulson Briefs President Bush on the New Terms of the AIG Bailout

Henry Paulson and Jim Lambright brief President Bush on new terms of the AIG bailout. As evidenced by the list below, the largest creditors of AIG were paid off at par courtesy of “Tiny” Tim Geithner. The list details the amount of money paid to various AIG counterparties via the AIG bailout - Societe General ($16.5-billion), Goldman Sachs ($14-billion), Deutsche Bank ($8.5-billion), Merrill Lynch ($6.2-billion) and UBS ($3.8-billion). These figures are not made public at the time of the bailout. (25)

Peter Schmidt

28 MAY 2018

ENDNOTES:

1. Saul Hansell and Kevin Muchring, "Derivatives - Just How Risky Are They," Institutional Investor, September 1992

2. John Succo, "Dear Lehman, Risk comes Full Circle," September 1998

3. Derivatives Strategy Magazine (Archive), June 1998

4. Roger Lowenstein, When Genius Failed, Random House, 2011, pp. 156-157

5. Lowenstein, p. 191

6. William A. Fleckensteinwith Frederick Sheehan, Greenspan's Bubbles - The Age of Ignorance at the Federal Reserve, McGraw-Hill, 2008, p. 51

7. Prepared testimony of Henry A. Paulson, Chairman and CEO Goldman Sachs, Securities and Exchange Comission hearing on the "Financial Marketplace of the Future," February 29, 2000

8. Chairman William H. Donaldson, Opening Statement at the SEC's April 28, 2004 Meeting

9. Michael Lewis, The Big Short, Penguin Books, 2010, 83

10. Henry Paulson, On the Brink, Hachette Book Group, 2010, pp. 43-46

11. James Grant, Mr. Market Miscalculates - the Bubble Years and Beyond, Axios Press, 2008, pp. 169-170.

12. Grant, pp. 173-176

13. Grant, pp. 179-180

14. Grant, p. 190

15. Grant, pp. 181-182

16. Lewis, p. 104

17. Lew, p. 212

18. Carrick Mollenkamp, Serena Ng, Liam Pleven, and Randall Smith, "Behind AIG's Fall, Risk Models Failed to Pass Real World Test," Wall Street Journal

19. Paulson, p. 61-62

20. "Behind AIG's Fall"

21. "Behind AIG's Fall"

22. Paulson, p. 185

23. Paulson, p. 241

24. Richard Teitelbaum and Hugh Son, "NY Fed's Secret Choice to Pay for Swaps Hits Taxpayers," October 27, 2009, Bloomberg

25. SIGTARP Report 10-003, "Factors Affecting Efforts to Limit Payments to AIG Counterparties," November 17, 2009