The Fed, Turning Japanese and the Shin Gin Ri

SUMMARY:

Often, the biggest consequence of Federal Reserve interest rate decisions isn't a consequence of the interest rate itself. Instead, its a consequence of how the changing interest rate impacts investor psychology. In the case of the 1920s and Tech Stock bubbles, the Fed created a new type of person - the "shin gin ri."

DISCUSSION:

The phrase "Turning Japanese" is often used to describe a specific economic environment; namely one characterized by enormous government deficits, central bank profligacy and slow growth. Of course, these characteristics have largely defined the Japanese economy since the crash of their enormous stock and real estate bubble. What some younger people may not realize is the ultimate origin of the phrase "Turning Japanese" was the 1980s new-wave band, The Vapors, and their song "Turning Japanese." (The song had nothing to do with economics. Instead the song was about alienation and how it made you feel like you were living in a foreign culture.)

There is an underappreciated aspect of 'turning Japanese' that is relevant to today's market. A huge factor in the Japanese bubble, and it is a factor found in every speculative bubble, was investor psychology. In a 1997 interview with the PBS show "Frontiline" investor Bill Fleckenstein was asked to explain why US stocks kept surging higher, even as by any historical measure of valuation stocks were richly priced. He answered by referencing what drove the Japanese stock bubble higher and higher;

"Because people are people. In Japan they have a name for this. They called them the 'shin gin ri,.' And it literally meant 'new human being.' They were the 20-something year-old people who had no experience in that market who were put in charge of all investing. And they thought that nothing would ever go wrong...People are buying stocks for one reason, they are going up."

When reviewing all the things the Federal Reserve has gotten wrong over the years it is easy to focus on interest rates alone. After all, it is by manipulating interest rates that the Fed attempts to direct the US economy to some desired outcome. However, in many cases the direct impact from the Fed cutting rates pales in comparison with the psychological impact from the rates cuts. This mechanism of rates cuts sparking a mania by impacting investor psychology can be demonstrated by reviewing two examples from history;

- The Long Island Conference of Central Banks (July 1927)

- The Emergency Rate Cut After LTCM Collapsed (October 1998)

The Long Island Conference of Central Banks

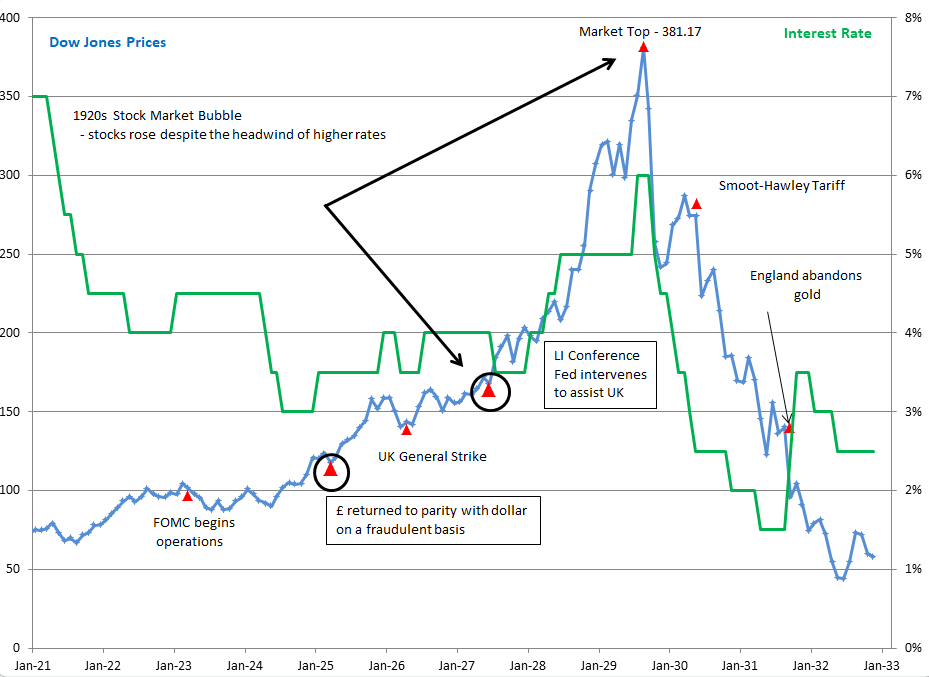

After World War I, the United Kingdom's economy was in shambles. As a result of the war, the UK had incurred debts to American banks - payable in dollars - that it could never pay back. As a consequence of these debts and overall lack of economic competitiveness, the pound lost more than 30% of its value against the dollar. Most significantly, New York had completely supplanted London as the world's financial capital. The UK did have one thing going for it, the governor of the Federal Reserve Bank of New York, Benjamin Strong, was a committed Anglophile. As the UK economy lurched from crisis to crisis, Strong resolved that bold action to assist the UK was called for. In July 1927, Strong took this bold action.

Strong called for a meeting of the world's central bankers on Long Island. The meeting had a single purpose - to coordinate a world-wide policy of "loose money" to advance the interests of England. The leaders of the central banks in France and Germany balked at the proposal. Strong dismissed the concerns expressed by France and Germany as well as the concerns expressed by many in the US banking establishment with the retort, that the interest rate cuts he had in mind would amount to little more than "a little coup de whiskey for the stock exchange." (2)

Of course, the animal spirits Strong thought would only run a little faster, ran completely wild. Strong became seriously ill and died in October 1928 at just 55-years old. In his absence, the Fed first tried a policy of 'moral suasion' to have banks stop loaning money for stock speculation . When that failed, they raised interest rates to reign in the stock market that was obviously spiraling completely out of control. It was to little avail and stock prices loosened themselves from any sort of rational basis. See Figure 1. At the valuations prevailing in October 1929, once selling began in earnest, the selling would soon feed on itself and prices would tumble - the market merely floated on a cushion of air blown by the Fed. The same animal spirits that saw stocks only going up would soon become consumed with man's most basic emotion - fear; and that fear would send prices tumbling.

FIGURE 1 - The Long Island Conference of July 1927 and the 1920s Stock Bubble

The Emergency Rate Cut After LTCM Collapsed (OCT 1998)

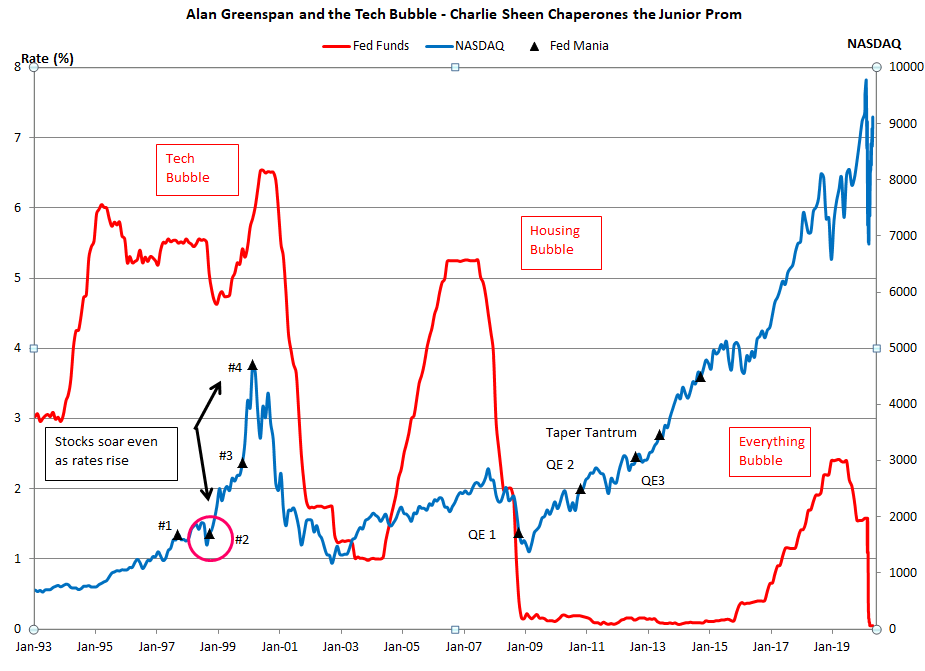

The precipitating cause of the Greenspan Fed cutting rates between scheduled FOMC meetings was the collapse of the hedge fund Long Term Capital Management (LTCM). LTCM seemed to have more MIT PhDs working for it than MIT. Basically, what the MIT educated geniuses of LTCM thought they could do is utilize computers to make a fortune by picking up pennies in front of runaway freight trains. LTCM gathered all sorts of statistics around prices and used this data to predict what prices should be. Anytime the market price differed from the computer predicted price, LTCM would make – by using highly complicated, highly leveraged financial derivatives – what were essentially bets or wagers that the market price would move to the price predicted by the computer.

Like any other highly leveraged financial exercise in picking up pennies in front of freight trains, LTCM's came to an end. In fact, the failure of LTCM is virtually identical to the much better remembered failure of AIG ten years later. (3) The failure of LTCM – which was acknowledged to have some of the smartest people in finance working for it - offered the real prospect of finally instilling some much-needed and long overdue discipline on Wall Street. The failure of LTCM could have been similar to a person swearing off even having a single drink before driving as a result of a near-miss accident while drinking drunk. However, and not unlike some overly indulgent uncle spoiling his favorite ne’er-do-well nephew even as the boy’s parents try to instill some sense of discipline and responsibility, Uncle Alan Greenspan intervened to save all his favorite nephews on Wall Street.

After cutting interest rates on September 29, 1998 – the first scheduled meeting of the FOMC after the LTCM bailout – Greenspan called a special meeting of the FOMC on October 15. At this meeting, Greenspan wanted to cut interest rates again. Greenspan was trying to mobilize the FOMC to get behind him to provide still more succor and support for Wall Street. Greenspan did have some resistance on the FOMC, most notably from Don Poole. Poole trenchantly asked, “Is there any chance the action today (cutting rates) could be viewed by some anyway as an effort to bail out the hedge funds?”

Those would prove to be famous last words. As Figure 2 makes clear, the emergency rate cut of October 1998 sparked an, until then, unprecedented speculative mania. The mania dwarfed even the one that Ben Strong conjured into existence in July 1927. At the time of the surprise rate cut the NASDAQ was at 1611, see #2 in Figure 2. In a little over a year, November 1999, the NASDAQ soared to 2967, a gain of 84%. In a final speculative blow-off the NASDAQ - doubtless fueled by the passage of the Citigroup Relief Act - reached 5000 in March of 2000, a 70% rise in just the four months since November, or over 210% since the surprise rate cut sixteen-months earlier in October 1998. The enormous move came with a considerable headwind provided by raising rates. Exactly as in the 1920s bubble, the rising rates of the 1990s proved no match for the animal spirits that Greenspan greatly encouraged.

Figure 2 - The Emergency Rate Cut of October 1998 and the Tech Stock Bubble

CONCLUDING REMARKS

The 1920s and Tech Stock bubbles saw their largest gains when interest rates were rising. Fed apologists routinely cite the 1920s and 1990s stock bubbles as proof the Fed can't be behind asset bubbles because they reached their greatest excesses when rates were rising. As demonstrated here, what really set markets soaring during these bubbles were the animal spirits that the Fed - in the persons of Ben Strong and Alan Greenspan - encouraged and emboldened. Once these animal spirits had been released by the Fed, rising rates weren't going to slow them down. The only thing that would stop these markets from marching higher would be these animal spirits simply exhausting themselves. IN both cases, once the market had exhausted itself, there was no remaining force large enough to keep the market from falling once the selling began in earnest.

Peter Schmidt

February 06, 2022

Sugar Land, TX

PS - As always if you like what you read, please consider registering with the site. It just takes an e-mail address, and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book! Registering with the site will give you access to the entire Confederacy of Dunces list as well as the Financial Crisis timeline. Both of these are a treasure trove of information on the crisis and the long-running problems that led to it.

Follow me on Twitter @The92ers

ENDNOTES:

1. Betting on the Market: Interview with Bill Fleckenstein

https://www.pbs.org/wgbh/pages/frontline/shows/betting/pros/fleckenstein.html

2. James Grant, Money of the Mind, Farrar Straus Giroux, New York, 1992, p. 192

3. The architects of LTCM were all MIT PhDs, while the architect of AIG's trade in mortgage derivatives was a Wharton finance professor, Gary Gorton. In both cases, while the financial rubble was still smoldering, the architects offered the same refrain; 'This was a completely unforeseen event, that couldn't be predicted.'