Great Depression Timeline: No, Ray Dalio, The Fed Didn't Raise Rates and Snuff Out a Recovery

SUMMARY:

- A myth - co-equal to the myth the Fed caused the Depression by being too passive - is the Fed exacerbated its Depression-era mistakes by tightening the money supply in 1937

- Ray Dalio, the hedge fund manager, and a Harvard professor endorsed this myth in March 2015

- A review of data from the 1930s reveals the Fed didn't tighten the money supply in 1937; instead, the Fed cut rates.

- The data from the 1930s also shows the banking system was awash in excess reserves.

- The huge volume of excess reserves proves there is no basis to conclude the Depression could have been avoided by the Fed creating even more banking reserves; the banking system already had more reserves than it knew what to do with.

DISCUSSION:

Over the past several weeks I have been discussing the Great Depression. One of the most enduring myths of the Great Depression was discussed in the blog post from November 10. (1) In particular, the theory that a thoroughly passive and predictably conservative Fed - wedded to old and incorrect ideas - caused the Great Depression by sitting idly by as prices collapsed. Of course, the biggest problem with this theory is that it fails to explain how the US was ever able to avoid anything remotely bad as the Great Depression when there wasn't even a Fed to take the actions it presumably should have taken after October 1929. Like most of what passes for economic insight today, the idea that the Fed caused the Depression by failing to be sufficiently active is completely at odds with both simple common sense and easily observable facts from the Depression era.

Another shibboleth from the Depression era - the perpetuation of which greatly empowers the Fed of today - is the equally bogus idea that the Fed greatly exacerbated the Depression by tightening the money supply by raising interest rates in 1937. In March 2015 - and to much fanfare - the hedge fund manager Ray Dalio discussed what he considered the Fed's huge mistake from 1937. Dalio was discussing the conundrum the Fed found itself in at the time. In a letter to his clients, Dalio admitted that he couldn't be sure of the correct time to raise interest rates, but he was sure that the Fed needed a 'Plan B' if it raised rates too early to ensure the Fed didn't repeat its policy mistakes of the 1930s;

"We don't know - nor does the Fed know - exactly how much tightening will knock over the apple cart. What we do hope the Fed knows, which we don't know, is how exactly it will fix things if it knocks it over. We hope that they know that before they make a move that could knock over the apple cart." (2)

Dalio's comments sparked a lot of discussion. Among those weighing in was Jeffrey Frankel, professor of 'capital formation and growth' - whatever that is - at Harvard's Kennedy School of Government. Frankel dismissed Dalio's concerns by claiming the economic environment of 2015 bore little resemblance to that of 1937. "I don't think we're in for a replay of 1937. The situation was pretty different. When the government prematurely re-enacted fiscal and monetary tightening back then, unemployment rates were still sky high." (3)

(Now that a Harvard professor dismissed any concerns I am sure we can all sleep better at night.)

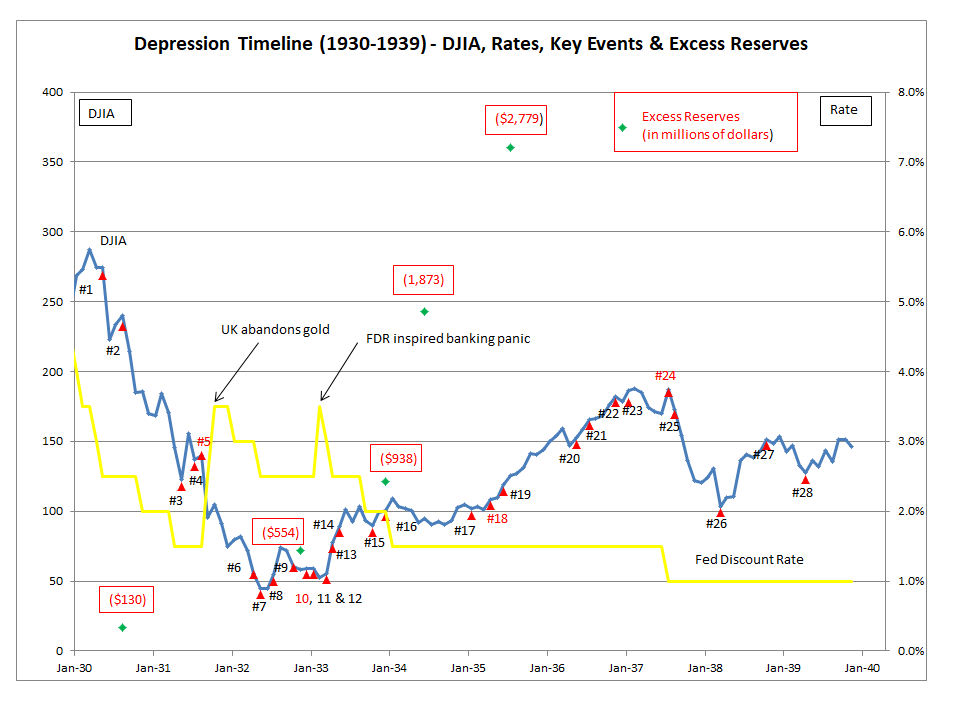

Remarkably, data from the time shows no tightening of the money supply by the Fed during 1937! See the chart below. The chart plots the DJIA (blue) and the Fed's interest rate on 'discounts and advances secured by eligible paper." (4) Not only does this chart put to lie the myth the Fed raised rates in 1937, the chart also shatters the fraud the Fed caused the Great Depression by being insufficiently active. In particular, note that the chart also plots - marked in red - excess reserves. These are reserves held by the banking system that are not then loaned to the investing public. Historically, banks would try to lend all their reserves; after all, banks have to pay interest on their reserves but are paid interest on their loans. (5)

As the chart makes clear, excess reserves soared during the Depression era. To put some perspective on the size of these excess reserves, the total for 1935 - $2,779-million - exceeded the total reserves in the banking system before the stock bubble crashed! As this data makes clear, the banking system of the Depression era was awash in reserves. How could the Fed be faulted for not creating even more reserves in the banking system when the banking system couldn't find borrowers for the reserves it already had. The only tightening performed by the Fed in the late 1937s was to increase the 'required reserve ratio' - the percentage of reserves that had to remain available for withdrawal. However, with the banking system already awash in reserves this wasn't tightening in any real sense. Indeed, as the chart shows, the Fed cut rates in 1937!

Another myth from the Depression era is that the New Deal worked. Like the myths around the Fed's purported inactivity (1) or its blunders (discussed here), the myth around the New Deal working supports today's powers that be. With the New Deal, the government greatly increased its involvement in the economy, and the scope of the Federal government greatly expanded beyond its clear proscriptions in the Constitution. A practical prerequisite for this greatly expanded role of government is the belief the New Deal worked. However, as next week's blog post will show the New Deal was a spectacular failure and the economy suffered a collapse in 1937 - see Item 24 in the chart - that was actually sharper than the one it suffered in October 1929!

Peter Schmidt

Sugar Land, TX

December 01, 2019

PS - As always, if you like what you read, please register with the site. It just takes an e-mail address and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book. Registering with the site will give you access to the entire Confederacy of Dunces list as well as the financial crisis timeline.

Help spread the word to anyone you know who might be interested in the site or my Twitter account. I can be found on Twitter @The92ers

ENDNOTES

1. http://www.the92ers.com/blog/fed-capitalizing-chaos-it-creates-timeline-great-depression

2. Harry Sender, Stephen Foley, and Sam Fleming. "Dalio Warns Fed of 1937 Style Rate Risk," Financial Times, March 17, 2015 https://www.ft.com/content/7a535d24-ccb7-11e4-b5a5-00144feab7de#ixzz3YLoT9SGR

(3) Nyshka Chandran, "Relax the Fed Isn't Risking a 1937-style Slump," March 17, 2015 https://www.cnbc.com/2015/03/17/relax-the-fed-isnt-risking-a-1937-style-slump.html

(4) The Board of Governors of the Federal Reserve, Banking and Monetary Statistics, 1914-1941. Washington, D.C., November 1943, pp. 441-442 https://fraser.stlouisfed.org/files/docs/publications/bms/1914-1941/BMS14-41_complete.pdf

(5) Excess reserves from, Benjamin Anderson, Economics and the Public Welfare, Liberty Press, Indianapolis, 1979 pp. 401-405.