Lawrence H. Summers - Archetypal Dunce Among the Confederacy of Dunces

Lawrence H. Summers is a walking, talking advertisement for this website. The basis of this website is provided by only two simple conclusions.

- The root cause of the financial crisis was a "purely human factor. This human factor is the completely false sense of omnipotence, self-importance and entitlement among the country's elite, as well as the nurturing of these beliefs at Ivy League colleges and other elite universities."

- Unless this purely human factor is addressed, "the US will be doomed to suffer other calamities every bit the equal of the financial crisis."

Recently, Lawrence Summers proved - beyond a shadow of a doubt - the veracity of these two conclusions.

The Financial Times published an article profiling President Trump's latest candidate for a position on the Federal Reserve, Judy Shelton, (1). Among the most conspicuous differences between Shelton and her potential future Fed colleages is she is completely dubious of the Fed's ability to accurately set interest rates. In fact, she likens the entire notion of the Fed being as actively involved in the economy as it currently is, as being little different than Soviet-style central planning! A position I both wholeheartedly agree with and endorse!

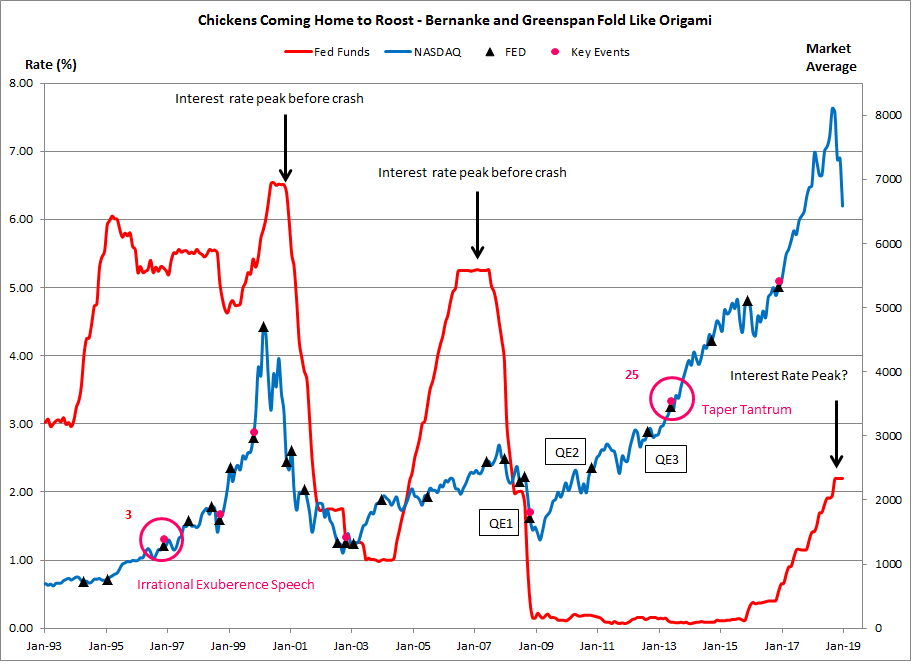

However, in response to the Financial Times article, Summers tweeted, "Judy Shelton does what I would have not thought possible. She falls well below Cain or Moore as a potential Federal Reserve governor. Hers would be a dangerous appointment." (2) In this tweet, Summers captures the enormous psychological defects that nearly all of the Confederacy of Dunces have. Summers speaks as if he had nothing to do with what has been happening in the country for the past thirty years, or as if the Fed has some sort of unblemished record of success, and was thus beyond reproach. As the bursting of two enormous bubbles, and the apparent bursting of a third - even larger bubble now - clearly show, all sorts of economic assumptions and central banking practices need to be revisited. See the chart, which has been published on the site several times before, for visual evidence of the obvious economic defects the country has suffered through for decades.

Summers is both completely blind to the obvious need to redress some clearly faulty economic assumptions and his massive role in the promulgation of these incorrect assumptions. Moreover, if Summers had any academic or intellectual integrity - which he most certainly does not - he would realize that Judy Shelton is hardly alone in her criticism of today's Federal Reserve, and its fatal, post-1971, infatuation with central planning via its Open Market Committee. Here is just a brief sampling of some of the well-respect economists and financiers who were deeply skeptical of a central bank assuming even a small fraction of the power the Fed currently has;

- Walter Bagehot, "In a crisis, a central bank can lend freely, but only against good collateral and only at high rates of interest."

- Dr. Benjamin Anderson, "The first four sources of capital - direct capitalization, (consumer saving), business thrift and, finally, taxation for capital purposes, are all wholesome, sound and safe. They have never been overdone; no country has ever gone wrong in creating capital these ways. The great troubles of the 1920s grew out of a fifth source of capital, namely new bank credit for capital purposes." (3) (i.e. a central bank creating bank reserves out of thin air)

- Wilhelm Ropke, "If in the production of goods the most important pedal is the accelerator, in the production of money it is the brake. To ensure that this break works automatically and independently of the whims of government and the pressure of parties and groups seeking 'easy money,' has been one of the main functions of the gold standard. That the liberal should prefer the automatic brake of gold to the whims of government in its role of trustee of a managed currency is understandable." (4)

- Fischer Black (of Black-Scholes option pricing fame), "I believe that in a country like the US, with a smoothly working fianncial system, the government does not, cannot, and should not control the money stock in any significant way. The government does, can only, and should simply respond passively to shifts in the private sector's demand for money. Monetary policy is passive, can only be passive and should be passive. The pronouncements of the Federal Reserve Board on monetary policy are a charade." (5)

All the people quoted here are completely sympathetic to Judy Shelton's skepticism of not just the ability of the Fed to set interest rates, but the enormous dangers inherent with the Fed attempting to do so. Moreover, the dust still hasn't finished settling from the collapse of the housing bubble! Yet Summers can still haughtily claim it is Judy Shelton that is dangerous and the Fed isn't some sort of menace?

The facts surrounding all this are completely clear, and a psychologically healthy person would have no problem seeing them. In particular, the time has long since passed when all of the operating assumptions around the Federal Reserve's Open Market Committee need to be revisited. That Lawrence Summers - with his degrees from Harvard and MIT, and his Wall Street millions - can't draw the correct conclusions from such obvious facts proves he is the danger, not Judy Shelton. He also proves the two foundational conclusions on my website are completely correct.

Peter Schmidt

Sugar Land, TX

June 02, 2019

PS - As always if you like what you read, please consider registering with the site. It just takes an e-mail address, and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book! Registering with the site will give you access to the entire Confederacy of Dunces list as well as the Financial Crisis timeline. Both of these are a treasure trove of information on the crisis and the long-running problems that led to it.

Also, follow me on Twitter @The92ers

ENDNOTES:

(1) James Politi, "Fed Candidate Slams Bank's Soviet Power Over Markets," Financial Times, May 31, 2019 https://www.ft.com/content/46c4b186-8308-11e9-b592-5fe435b57a3b

(2) To which I tweeted Summers, "Hers would be a dangerous appointment." So says one of the biggest financial terrorists of all time. https://twitter.com/The92ers/status/1134490963555102722

(3) Benjamin M. Anderson, Economics and the Public Welfare, Liberty Press, Indianapolis, 1979, p. 133

(4) Wilhelm Ropke, Economics of a Free Society, Ludwig von Mises Institute, Auburn, AL 2008, p. 100

(5) http://www.the92ers.com/blog/fatal-conceit-economics-source-todays-economic-chaos-and-question-never-asked