Normalization of Deviance and Central Banks: What They Were and What They've Become - Part III

Despite what all our supposed betters in the European Union and their proxies among the elite in this country are constantly lecturing to us, the French Revolution wasn't a triumph of the intellect and reason. It was a triumph of terror and the fanatical zeal which motivated it. As such, the French Revolution was a harbinger of the modern political movements that followed in its wake. Like all the totalitarian regimes of the 20th century, the French revolutionaries assigned no value to the lives of people not willing to completely subject themselves to the universal ideals at the vanguard of the revolutionary movement. Maximilien Robespierre said it best in his 'Republic of Virtue' speech, "Terror is nothing other than prompt, severe, inflexible justice." Of course, the most obvious manifestation of Robespierre's sense of justice was the Reign of Terror.

Even after tens of thousands had already died at the hands of the revolutionaries, their kangaroo courts and their instrument of execution, the guillotine, their bloodlust and zeal both remained unslaked. The murderous madness reached its zenith in July 1794. It was then that a handful of nuns and lay women were executed for refusing to submit to the Civil Constitution of the Clergy. As the sixteen women were led to the guillotine to be executed one by one, they all continued to sing religious hymns and to pray. (1) It was an amazing demonstration of faith and strength, the impact of which would soon be felt across revolutionary France. Many people began to realize no amount of blood would ever satisfy the zeal of Robespierre and the other members of the 'Committee of Public Safety' (2). Approximately a 'decade,' ten days, (3) later, Robespierre and his henchmen were arrested and executed soon after.

ERA III - The Greenspan/Bernanke Era; The Die is Cast

The reign of Alan Greenspan and Ben Bernanke at the Fed lasted from 1987 through 2014. These years were a reign of financial terror that is the economic equivalent of the political terror unleashed by the Jacobins in revolutionary France. However, while the violence unleashed by the Jacobins ultimately consumed the Jacobins themselves, the economic idiocy and blundering of the Greenspan/Bernanke Fed led to the Fed assuming powers few would have ever conceived possible - at least in a free country.

The Greenspan/Bernanke era at the Fed is the most crisis-riddled period in US economic history. During those 28-years, three enormous, economy altering bubbles blew up, two of which have already completely collapsed. In addition, wealth - and the power which wealth can effortlessly dispatch - became concentrated like never before. Indeed, the Greenspan/Bernanke era proved as a gospel truth the veracity of Andrew Jackson's warning about an unassailable central bank. Namely, that such a bank would make "the rich richer, and the potent more powerful."

The disastrous outcomes of this era were the ineluctable consequences of the disastrous actions taken by Greenspan and Bernanke, with the actions themselves the product of their completely muddled thinking. What follows is a brief description of one disastrous action and one muddled thought. Specifically;

- Alan Greenspan cutting rates between FOMC meetings after LTCM collapsed

- Bernanke's Total Misunderstanding of Inflation

Alan Greenspan and Long-Term Capital Management (LTCM)

LTCM was a hedge fund. LTCM gathered all sorts of statistics around prices and used this data to predict what prices should be. Anytime the market price differed from the computer predicted price, LTCM would make – by using highly complicated, highly leveraged financial derivatives – what were essentially bets or wagers that the market price would move to the price predicted by the computer. Because the spreads or difference between the prices predicted by the computer and the prices prevailing in the market were often very small, the only way to make serious money using this strategy was to use enormous leverage. Some idea of the leverage LTCM used can be gleaned by understanding that it was not unusual for LTCM to have $30 of borrowed money invested for each $1 of its own capital invested. With this amount of leverage, a trading loss of approximately 3% will result in insolvency.

Some idea of the complexity - and the enormous intellectual arrogance - behind LTCM's mathematical models can be gleaned by a review of the educational background of some of LTCM's partners. Greg Hawkins, Larry Hillibrand, William Krasker, Robert Merton, David Mullins and Eric Rosenfield all had PhDs from MIT. Merton was also a professor at MIT and won the Nobel Prize in economics. Rosenfield and Mullins both taught at Harvard, and Mullins was also vice-chair of the Federal Reserve. (Mullins was replaced at the Fed by Alan Blinder, Dunce #5.) The mistake all these MIT educated geniuses tripped over was merely the first rule of counting cards. LTCM made enormously large bets via their derivatives contracts. However, the basis of their bet - their mathematical models - was never accurate enough to justify the high leverage they routinely used. It didn't matter that LTCM's models were correct 90% of the time when it only took a 5% level of inaccuracy for the firm to collapse!

In other words, don't be fooled by the all the MIT PhDs earned by the partners at LTCM. LTCM's business model was essentially to use computers to pick up pennies in front of runaway freight trains. After a few years of enormous success, LTCM began to suffer enormous losses. Because of its early successes, LTCM had been able to borrow huge amounts of money. As it teetered on the brink of solvency in September 1998, it was estimated that LTCM may have had as much as $1-trillion in market exposure through its various derivative trades. As is the Fed’s want to do, the Fed organized a bailout of LTCM.

The failure of LTCM – which was acknowledged to have some of the smartest people in finance working for it - (albeit that is not saying much) – offered the real prospect of finally instilling some much-needed and long overdue discipline on Wall Street. The failure of LTCM could have been similar to a person swearing off even having a single drink before driving as a result of a near-miss accident while drinking drunk. However, and not unlike some overly indulgent uncle spoiling his favorite ne’er-do-well nephew even as the boy’s parents try to instill some sense of discipline and responsibility, Uncle Al intervened to save all his favorite nephews on Wall Street.

After cutting interest rates on September 29, 1998 – the first scheduled meeting of the FOMC after the LTCM bailout – Greenspan called a special meeting of the FOMC on October 15. At this meeting, Greenspan wanted to cut interest rates again. Apparently, Uncle Al didn’t think organizing the LTCM bailout and cutting rates once was enough support for Wall Street. Greenspan was trying to mobilize the FOMC to get behind him to provide still more succor and support for Wall Street. Greenspan did have some resistance on the FOMC, most notably from Don Poole. Poole trenchantly asked, “Is there any chance the action today (cutting rates) could be viewed by some anyway as an effort to bail out the hedge funds?”

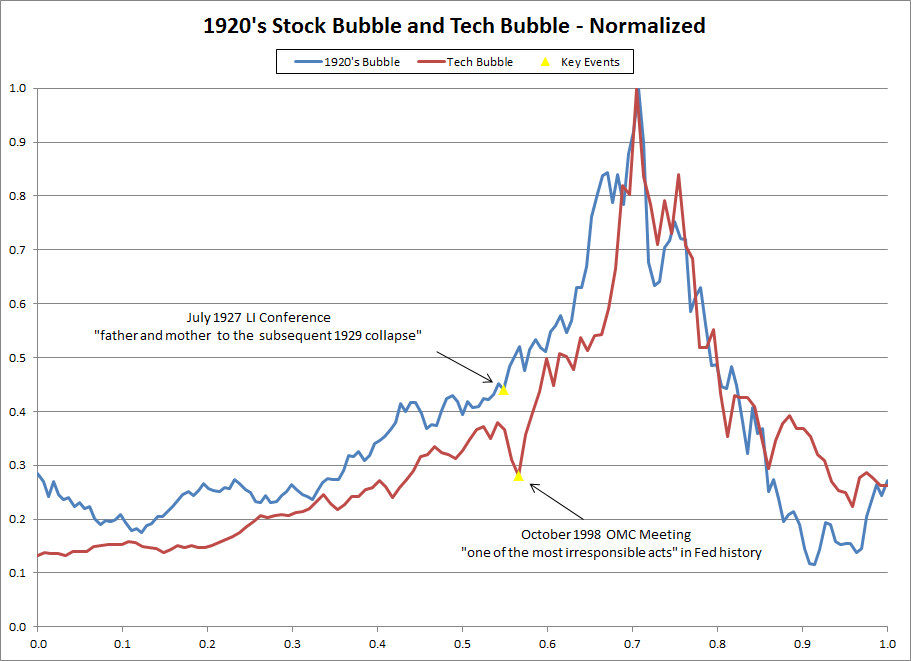

As it turned out, it was a 100% certainty that the October rate cut would be viewed as an effort to bail out hedge funds. Speculators all over Wall Street became convinced that no matter how recklessly they acted, there was a limit to how bad things would get. If things started to even look like they might become bad, then Uncle Al and the Fed would bail them out. This mindset became known as the “Greenspan put.” The “Greenspan put” was a financial backstop for all of Wall Street and, not surprisingly, Wall Street acted completely recklessly as a result. In the case of the October 1998 rate cut between scheduled FOMC meetings, a manic sense of “irrational exuberance” clearly engulfed Wall Street. At the time of the surprise rate cut the NASDAQ was at 1611. In a little over a year, November 1999, the NASDAQ soared to 2967, a gain of 84%. In a final speculative blow-of the NASDAQ reached 5000 in March of 2000, a 70% rise in just the four months since November, or over 210% since the surprise rate cut sixteen-months earlier in October 1998.

The stock market climax run following the October 1998 rate cut was a case of history repeating itself, and eerily similar to the stock market blow-off that followed the July 1927 Long Island conference of central bankers, see the discussion under Era I. The chart plots the 1920’s stock bubble for the period January 1920 – September 1933 and the tech bubble for the time period from January 1993 – March 2003. The data in the chart is “normalized.” Normalization is a technique commonly used in statistics when evaluating data measured over different lengths of time that is also measured using different scales of magnitude.

As the chart shows, the disastrous impacts from Ben Strong's 'coup de whiskey' to benefit the UK, (July 1927) and Alan Greenspan cutting rates to benefit Wall St. and hedge funds (October 1998) were virtually identical. In both cases, the Fed cast aside its original 'passive' reason for existence and exercised discretion to achieve goals nowhere to be found in its original mandate. In both cases, these actions led to a fantastic asset bubble that was destined to crash back to the earth with long-term consequences.

Ben Bernanke's Total Misunderstanding of Inflation

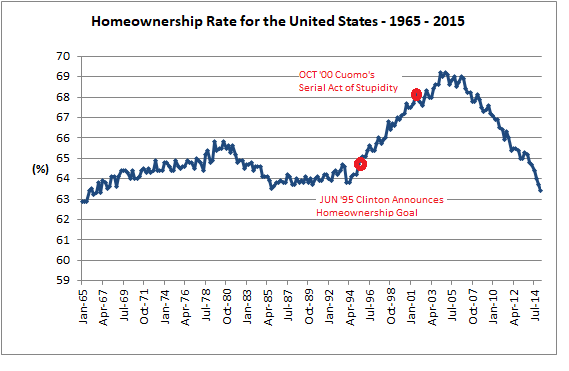

The enormous bubble in stocks that Greenspan's 1998 emergency rate cut sent rocketing to outer space was destined to collapse in exactly the same way that Ben Strong's stock bubble had. After the tech stock bubble crashed, the Nasdaq bottomed in October 2002 after falling nearly 80%, Greenspan - now working with Bernanke - slashed rates. Rates fell to levels never seen before and stayed there for years on end. These low rates - acting in concert with President Clinton's 'strategy' to increase homeownership to 67.5% - sent home prices soaring. In October 2000, Andrew Cuomo, then HUD secretary, directed the two mortgage giants, Fannie and Freddie, to issue 50% of their mortgages to low and moderate income borrowers. This act of stupidity made a housing collapse inevitable; it was only a matter of how big the collapse would be. Courtesy of the Greenspan and Bernanke Fed, the housing collapse would be world-altering.

In terms of homeownership, the housing bubble peaked in April 2004. The Fed didn't start raising interest rates until July 2004. In July 2004, rates were just 1% and had been below 2% since December 2001. Fueled by these low rates and the economic idiocy in President Clinton's 'strategy' to boost homeownership, home prices had soared to unsustainable levels. Amazingly, as home prices soared for years on end, Bernanke and Greenspan constantly claimed there was little or no inflation. Given that housing is such a large expense to the average family, how could Greenspan and Bernanke claim there was no inflation when home prices were soaring?

The answer to this question can be found in a speech that Bernanke gave on November 08, 2002. The speech was in honor of Milton Friedman’s ninetieth birthday. (4) In this speech, Bernanke provides his – and Friedman’s - theory of the Great Depression. Friedman concluded the Fed caused the Great Depression by allowing the money supply to collapse during the 1930s. In his analysis, Friedman first attempts to show those times – Bernanke calls them “monetary policy episodes” - during the Depression era when the money supply changed for reasons “plausibly unrelated to the state of the economy.” With these episodes identified, Friedman reasoned it would then be possible to determine how changes in the money supply caused changes in the economy. The Friedman thesis purports to show the Great Depression can “reasonably be described as having been caused by monetary factors,” or changes in the money supply drove changes in the economy. When the money supply fell the economy slumped. When the money supply increased, the economy recovered.

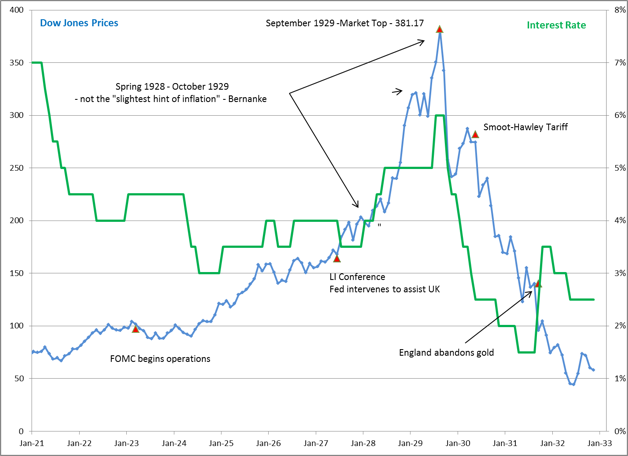

What the Friedman analysis of the Great Depression – and Ben Bernanke’s endorsement of it in November 2002 – really shows has nothing to do with the Depression. Instead, the analysis and Bernanke’s endorsement of it exposes what is the Fed’s overarching blunder of the Greenspan/Bernanke era – the failure to understand one word, inflation. The first “monetary policy episode” Bernanke cites as proof the Fed caused the Great Depression was the policy tightening that began in the spring of 1928. (At the time Ben Strong was incapacitated by illness and the Fed desperately tried to unwind the mistakes Strong had had made after the July 1927 conference of central bankers.) Bernanke criticizes the Fed for raising interest rates during this period because – in his opinion – there wasn’t “the slightest hint of inflation.”

While the Fed had acted recklessly and far beyond its mandate to intervene in credit markets to advance the interests of the UK, consumer prices had changed very little during the 1920s. Because of this, Bernanke – and Friedman, as well as almost PhD economists – conclude there was no inflation in the 1920s. (5) Unfortunately for their analysis there were a variety of secular trends – primarily the Industrial Revolution – that produced enormous increases in productivity, and these helped to keep consumer good prices down in the 1920s. Where the Fed’s unwarranted increase in the money supply, the classical definition of inflation, manifested itself was in the price of assets – stocks and real estate in particular.

See the chart above and the period from spring 1928 to October 1929. Note stock prices rising to the stratosphere. (Stock prices are in blue and interest rates are in green.) This is what Ben Bernanke means - foolishly it hardly needs to be added - when he says "not the slightest hint of inflation." As the chart makes clear, even with the benefit of hindsight Ben Bernanke completely misdiagnosed the 1920s stock bubble. Ben Bernanke relies on an artificially narrow definition of inflation that is confined to consumer prices, and this makes him blind to inflation as measured by even huge increases in asset prices. In fact, stable consumer prices are no proof that credit is not being expanded too liberally or the risk of a financial bubble is low. Indeed, financial bubbles are most likely to occur when goods prices are relatively stable – the Great Depression and the Financial Crisis of 2008 provide ample evidence of this. In his misdiagnosis of the 1920s stock bubble Ben Bernanke exposes exactly the same mindset that made him and the Federal Reserve blind to the enormous risks associated with the ballooning costs of homes in the early 2000s.

CONCLUDING REMARKS - PART III

The Greenspan/Bernanke era at the Fed is arguably the most crisis-riddled period in US economic history. This wasn't bad-luck or simply a reflection of how long this era lasted - an appallingly long 28-years. Instead, the crisis atmosphere that prevailed for huge lengths of the Greenspan/Bernanke era is merely a reflection of the huge blunders authored by Greenspan and Bernanke. In the discussion here, Greenspan's inexcusable emergency rate cut after LTCM's collapse and Bernanke's blindness to inflation as measured by increases in asset prices merely scratch the surface of everything wrong with the Fed of this era. While it is important to catalog the myriad blunders of the Greenspan/Bernanke era, it is also important not to lose the forest for the trees. The root cause of these blunders isn't addressed by correcting economics curricula at Harvard and MIT, or tweaking the Fed's computer models of the economy. Instead, the root cause is addressed by revisiting the notion of investing so much power in the hands of so few people.

This discussion began by likening the Greenspan/Bernanke era at the Fed to a financial reign of terror. However, unlike the political reign of terror that animated the French Revolution and ultimately consumed itself, the financial reign of terror of the Greenspan/Bernanke era proved to be a great benefit to the Fed as an institution. Instead of suffering rebuke and undergoing a long overdue reform for the many obvious blunders committed by its chairman, the Greenspan/Bernanke era saw the Fed accumulate power that no one would have even judged imaginable just a few years before. In other words, as the Fed continued to make larger and larger mistakes with increasingly grave consequences, the Fed accumulated more power. Exactly how much more power would be evident in the wake of the housing bubble collapse and will be discussed in Part IV.

Peter Schmidt

Sugar Land, TX

May 03, 2020

PS - As always, if you like what you read, please register with the site. It just takes an e-mail address and I don't share this e-mail address with anyone. The more people who register with the site, the better case I can make to a publisher to press on with publishing my book. Registering with the site will give you access to the entire Confederacy of Dunces list as well as the financial crisis timeline.

Help spread the word to anyone you know who might be interested in the site or my Twitter account. I can be found on Twitter @The92ers

ENDNOTES:

(1) Marie Antoinette faced the various indignities she was subjected to with the same grace and courage as the 'Martyrs of Compiegne.' Her husband, King Louis XVI, was executed in January 1793, and Marie Antoinette wasn't executed until October of that year. As some evidence of her great strength and grace, as she was approaching the guillotine she accidentally stepped on the foot of her executioner. Her last words were then, 'Pardon me sir. I did not do it on purpose.' As far as the 'universal' nature of French Revolutionary ideals are concerned, one of the main reasons Marie Antoinette was executed was her Austrian heritage. Finally, it was Marie's husband, Louis XVI, and not the French revolutionaries who supported the American revolution. Modern France and francophiles everywhere routinely and intentionally confuse this history, and attempt to advance the notion that the French revolution provided great succor to the American revolution which preceded it!

(2) A name straight out of Orwell's 1984 or the Soviet Union.

(3) To show how farcical the French Revolution was, and what an inflated sense of self the people who led it had, an understanding of all the various aspect of life that the French Revolution attempted to remake is a good place to start. Included among these aspects was the humble calendar. Weeks would now have ten days, a 'decade,' instead of seven. This had the convenient benefit of eliminating Sunday, the traditional day of rest and religious celebration. Months had three 'decades' and there were twelve months in the year. The five remaining days were then merely added to the end of the year to keep the calendar somewhat close to the actual solar year. Year 1 in the French Revolutionary calendar began with the dissolution of the monarch in 1792. Clowns - the lot of them.

4. https://www.federalreserve.gov/BOARDDOCS/SPEECHES/2002/20021108/