Reprint: June 05, 1995 - President Clinton Formally Kicks-off the Housing Bubble

This is a re-print of a blog post that ran one year ago this week. President Clinton's speech from June 5, 1995 is discussed. The policies and objectives laid out by President Clinton in this speech played an enormous role in the housing bubble and, by extension, all of the Federal Reserve's monetary policy interventions that came in the wake of the housing bubble's collapse. It is no exaggeration to say that the United States is still living with the repercussions of this speech. I substituted a different chart for the one included in the original blog post. This new chart does a better job of demonstrating the enormous role President Clinton's speech played in everything that came after. (Peter Schmidt, June 09, 2009)

SUMMARY

- On June 5, 1995, President Clinton announced an ambitious homeownership goal for the country - to three significant digits no less - 67.5%.

- This was economics by fiat and central planning.

- The goal would be achieved, but - like all sorts of production goals set in the Soviet Union - achieving the goal would wreck the economy.

- The goal was considerably higher than any previous homeownership rate and would require enormous changes to the housing market.

- These changes - which were the result of government meddling in what should be a private affair, lending - greatly increased the risk of mortgage defaults

- Through his housing secretary, Henry Cisneros, President Clinton was able to utilize the government's "mailed fist in the velvet glove" to enlist support from private sector.

- Cisneros would also direct the two government sponsored enterprises - Fannie Mae and Freddie Mac - to completely alter their business practices to achieve the 67.5% goal.

- President Clinton claimed that achieving this goal was one of the most important things his administration could do.

- To achieve this goal, the Clinton Administration came up with "one-hundred specific actions;" these now read like step-by-step instructions how to destroy the US economy.

- Not mentioned by President Clinton - but crucial to both achieving the 67.5% goal and causing the financial crisis - was the ultra-low interest policy of the Greenspan/Bernanke Fed.

DISCUSSION

On June 5, 1995 President Clinton publicly discussed the benefits of his "Home Ownership Strategy." This strategy - which was nothing more than central planning - came, ironically enough, just a few years after the collapse of the largest practitioner of central planning - the Soviet Union. How did the Clinton administration ever think they could discern what the homeownership rate in the country should be? Where did the goal of 67.5% come from? If 67.5% is good, why not something higher? Writing in his survey of US economic history, Dr. Benjamin Anderson - a banker in the traditional sense - noted, "The substitution of government policy in credit matters for the free exercise of banking judgement is one of the most dangerous things that can come to a country." (1) In order to achieve its 67.5% goal, the Clinton Administration would interfere in the mortgage market in an unprecedented way and thus prove the veracity of Dr. Anderson's warning.

The following are excerpts from President Clinton's speech on June 05, 1995. The text of the entire speech is available from UC Santa Barbara's American Presidency Project, (2).

"...You want to reinforce family values in America, encourage two-parent households, get people to stay at home. Make it easy for people to own their own homes and enjoy the rewards of family life and see their work rewarded. This is a big deal. This is about more than money and sticks and boards and windows. This is about the way we live as a people and what kind of a society we're going to have...."

"And I cannot say enough in terms of my appreciation to Secretary Cisneros, who is a genuine visionary...Since the day I asked Secretary Cisneros to build this strategy, he has done about everything a human being could do. And I can say this without knowing that I'm overstating it, that if we succeed in doing this, if we succeed in making that number (67.5%) happen, it will be one of the most important things this administration has ever done, and we're going to do it without spending more tax money....We have to remember that there are millions of people just like them (people on stage with the president) who believe that homeownership is out of reach...Now we have begun to expand it (homeownership). Since 1993, nearly 2.8 million new households have joined the ranks of America's homeowners, nearly twice as many as in the previous two years. But we have to do better..."

"The goal of this strategy , to boost homeownership to 67.5% by the year 2000, would take us to an all-time high, helping as many as 8-million families cross that threshold...I want to say this one more time, and I want to thank again all the people here from the private sector who have worked with Secretary Cisneros on this. Our homeownership strategy will not cost the taxpayers one extra cent. It will not require legislation. It will not add more Federal programs or grow Federal bureaucracy, its one-hundred specific actions that address the practical needs of people who are trying to build their own personal version of the American dream..."

Of course, President Clinton's outlook for what the future held because of his homeownership "strategy" proved wildly optimistic. To be sure, the strategy did not require one extra cent. Instead, it ultimately required hundreds of billions of dollars being funneled directly and indirectly to the largest banks in the country. The Federal Reserve - who also has much to answer for in the formation of the housing bubble - expanded its balance sheet by nearly $4-trillion dollars in the aftermath of the housing collapse. The Fed created enormous amounts of money out of thin air to purchase all sorts of distressed assets from banks up and down Wall Street.

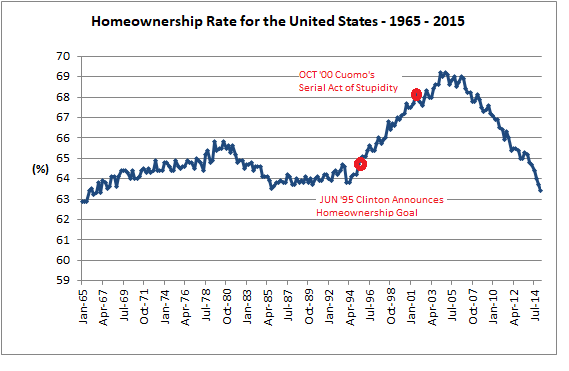

Amazingly, President Clinton's central plan to increase homeownership ultimately didn't do much to expand homeownership! To be sure, the homeownership rate did greatly - and temporarily - increase to over 69% in April 2004. However, in the aftermath of the financial crisis, the homeownership rate collapsed and went back to levels seen 50-years ago. See the chart below, homeownership data is from the St. Louis Fed (3). Also highlighted in this chart is Andrew Cuomo's decision - he was HUD secretary at the time - to have 50% of GSE mortgages go to low and moderate income borrowers. This decision sealed the economic fate of the United States.)

Finally, anybody who doubts what should be the obvious role of the Clinton Administration in the housing bubble should familiarize themselves with what become of HUD Secretary Cisneros. After leaving government "service," Cisneros become a real estate developer and sat on the board of the largest mortgage lender in the US, Countrywide. (Kathleen Brown, the sister of California governor, Jerry Brown, was also on the board.) Cisneros' signature development in his hometown of San Antonio, Lago Vista, spewed an enormous number of foreclosures, divorces and social chaos. Even the New York Times was forced to admit, that the only thing Cisneros built wasn't houses, but "flawed American dreams." (4)

Peter Schmidt

10 JUN 2018

Re-issued: 09 JUN 2019

ENDNOTES:

(1) Dr. Benjamin Anderson, Economics and the Public Welfare, Liberty Press, Indianapolis, 1979, p. 176

(2) University of California at Santa Barbara, The American Presidency Project, William J. Clinton, "Remarks on the National Homeownership Strategy," June 5, 1995 http://www.presidency.ucsb.edu/ws/?pid=51448

(3) Federal Reserve Bank of St. Louis, Homeownership Rate for the United States, https://fred.stlouisfed.org/series/RHORUSQ156N

(4) David Stretfeld and Gretchen Morgenson, "Building Flawed American Dreams," New York Times, October 18, 2008