Bill Clinton

The economy and high finance are not nearly as complicated as MIT PhD economists routinely make them out to be. To be sure, neither can be captured in the ridiculous equations these educated fools have come up with. The first British economist to win the Nobel Prize, Sir John Hicks famously defined “really catastrophic depressions,” not with complicated equations but with common sense insight. Hicks defined depressions as those occasions where “the rot in the financial system goes very deep.” Rot in a financial sense simply means bad loans. There was nothing fiendishly complex about the financial crisis. The financial crisis was the inevitable consequence of so many housing related loans – and Wall Street “side bets” on these loans – going bad.

The Clinton administration is singularly responsible for creating the environment where enormous volumes of bad loans were essentially required to be made. Despite the enormous damage it caused, the genesis of the financial crisis is completely straightforward to understand;

- The Clinton Administration created a gigantic engine of economic destruction through its establishment of a 67.5% homeownership goal for the country.

- The Federal Reserve - through its unprecedentedly radical interest rate policies and years of backstopping Wall Street - poured nitromethane into this engine.

- Wall Street banks - largely by ignoring both their fiduciary responsibilities and simple human decency – pawned off all sorts of complicated, toxic mortgage debt instruments on an unsuspecting public and each other, and turned the ignition key to this engine.

As with both Ben Bernanke (#3) and Alan Greenspan (#29), the contributions of the Clinton Administration to the housing bubble are enormous and difficult to distill into any sort of summary. Fortunately, the always garrulous Bill Clinton provided plenty of speeches throughout the 1990s where he bragged about the accomplishments of his housing program and all the great things it would bring in the future. Here is Bill Clinton in June 1995 describing what his housing strategy was and what little it would take from taxpayers to achieve the objectives of this strategy.

“The goal of this strategy, to boost homeownership to 67.5% by the year 2000, would take us to an all-time high, helping as many as 8-million American families cross that threshold…I want to say this one more time, and I want to thank again all the people here from the private sector who have worked with Secretary Cisneros on this: Our home ownership strategy will not cost the taxpayers one extra cent. It will not require legislation. It will not add more Federal programs or grow Federal bureaucracy. It’s one-hundred specific actions that address the practical needs of people....”

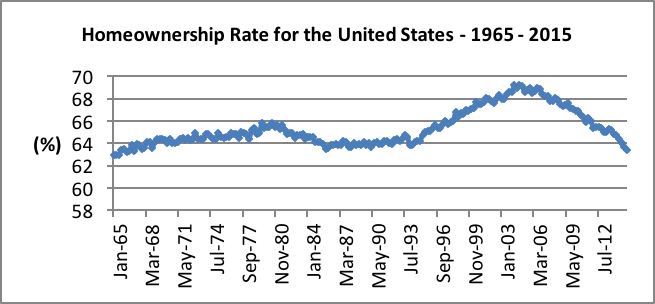

The “one-hundred specific actions” Clinton came up with to increase homeownership levels to 67.5% now read like step-by-step instructions on how to destroy the US economy. I recognize that President Clinton has a Yale law degree, but how he was so smart to come up with a national housing goal – to three significant digits no less – when this goal greatly exceeded any homeownership level in the past is anyone’s guess. For some idea of just how unprecedented a 67.5% homeownership rate was, see the chart below, data from the St. Louis Fed;

The simple – if unpleasant - fact to President Clinton’s legion of admirers is he created a central plan for housing. A national goal for homeownership, particularly one that would take it well beyond the levels seen at any time in the country’s history, is no different than some communist party official from the 1980s deciding fertilizer production targets for Cherkassy and pig iron production goals for Kharkov. A variety of circumstances will affect an individual family’s desire to purchase a home. These circumstances can ebb and flow, and in isolation one homeownership level shouldn’t be considered better than another. More significantly for the development of the housing crisis, no individual is capable of ever discerning what the ideal homeownership level of the country should be.

However, Bill Clinton wanted to be president since he was a teenager. With this psychological background, once elected president, whatever Bill Clinton ever had in terms of modesty and humility were long since gone from his mindset. In the Greek tragedies of antiquity, it was always pride that was the tragic hero’s ultimate undoing. Many theologians, including St. Augustine, contend that the sin of pride is the cardinal sin because it is the sin from which all other sins flow. More recently, another theologian, Søren Kierkegaard, expanded on the devastating consequences of pride, “The proud person always wants to do the right thing, the great thing. But because he wants to do it in his own strength, he is fighting not with man, but with God.”

It is this completely false sense of hubris and pride that plays an enormous role in the constantly recurring and disastrous attempts of Western elites everywhere to centrally plan, manage and control things completely incapable of their central control. (Under communism, the desire to centrally plan was rooted in the more primal instinct of the naked quest for power, not pride.) Nowhere is the Western political elites’ cardinal sin of pride more evident than in the central plan Bill Clinton pursued for housing. Bill Clinton thought he could bend the housing market to his will. He was wrong and tens of millions of people suffered the economic consequences.

From time to time, apologists for the Clinton administration are forced to defend Bill Clinton and advance the argument that Bill Clinton’s central plan for housing didn’t have anything to do with the crash of the housing market. Of course, any such argument is patent nonsense. That said – and in spite of the epic economic ignorance of President Clinton along with his two HUD secretaries, Henry Cisneros (#11) and Andrew Cuomo (#16) – it is only fair to point out the Clinton administration was not solely responsible for the housing crash and financial crisis. Wall Street, the Federal Reserve, Ivy League economic departments and elite universities generally all played enormous roles in allowing the economic cancer latent in Bill Clinton’s central plan for housing to metastasize and spread to the country’s economic heart and lungs.

Additional Information:

See Henry Cisneros (#11) and Andrew Cuomo (#16) for the rubber of President Clinton’s central plan for housing hitting the proverbial road. See Shaun Donovan (#18) for more information on the pathetic and weak arguments advanced to defend Bill Clinton from well-deserved blame for the financial crisis. For all the congressional support provided to President Clinton’s housing central plan see Kit Bond (#6), Barney Frank (#21), Gregory Meeks (#35) and Maxine Waters (#47). See Lawrence Summers (#45) for the critical role “side bets” - in the form of financial derivatives – on the mortgage market played in the financial crisis.