Lawrence Summers

Lawrence Summers shares many things in common with Robert Rubin (#41), not the least of which is an enormously flawed character. Exactly like Rubin, Summers would be at the center of enormous and easily discernible blunders in judgement that directly led to the crisis. Nevertheless, even after the financial crisis hit and caused enormous damage, Summers continued to consider himself an “expert” in economics. He continued to offer advice on all sorts of economic topics his role in causing the crisis clearly shows he knows nothing about. Completely unsurprisingly, the political, media and Wall Street establishments – all of whom also have much to answer for concerning the financial crisis’ origins – share the opinion of Lawrence Summers that Lawrence Summers has of himself. Despite his obvious role in causing the crisis, after the crisis Summers was made an economic advisor to President Obama, wrote several high-profile editorials in the New York Times and Washington Post and still consults with hedge funds. Don’t be confused by the establishment’s take on Lawrence Summers; Lawrence Summers is a dunce.

Summers’ role in the crisis is inextricably linked to the critical role derivatives played in the financial crisis. Derivatives are not typical investments like stocks or bonds that are, themselves, assets. Instead, derivatives “derive” their value from some other asset. During the housing bubble, an enormous industry had developed around derivatives tied to mortgage bonds. These derivative investments were essentially little more than “side bets” on whether an individual mortgage bond would remain solvent or not. AIG, relying on models developed by a Wharton finance professor, Gary Gorton (#27), was the biggest player in derivatives tied to mortgage bonds and would lose tens of billions of dollars when the housing bubble collapsed.

As far as understanding Summers’ critical role in the financial crisis is concerned, the most important thing to understand about derivatives – linked as they are to Summers - is far more money was likely lost on derivatives going bad then mortgage loans going bad. In other words, without all the derivative side bets going bad, there probably wouldn’t have been a financial crisis in the first place. To be sure, even without the impact of failing derivatives, the economy would have suffered a serious setback as a result of the housing bubble bursting and the enormous numbers of failing mortgages. However, it is unlikely that anything resembling the financial crisis would have occurred.

The market for derivatives didn’t grow as large as it did by chance; it grew as large as it did because powerful people wanted the market for derivatives to grow. Lawrence Summers in particular is a primary reason the derivative market became as large as it did. The influence Lawrence Summers exerted to make the market for derivatives so large makes Lawrence Summers – along with Ben Bernanke (#3), Bill Clinton (#12), Andrew Cuomo (#16), Barney Frank (#21) and Alan Greenspan (#29) – one of the very few key catalysts for the entire financial crisis.

Surely, and given the enormous role played by complicated derivative investments in the crisis, one of the major milestones on the road to the financial crisis must be the July 1998 congressional hearings on derivatives. These hearings were called because of Brooksley Born’s modest proposal from May 1998 to regulate the trade in derivatives. At the time, derivatives were largely unregulated and derivative positions were often recorded “off the balance sheet.” In other words, while regulations existed – namely the net capital rule, see William Donaldson (#17) - to limit the amount of leverage banks could employ, these limits on leverage could easily be avoided by using derivatives. As a result, highly leveraged positions could be established with derivatives that couldn’t be taken with other investments.

In the halcyon days of a passive central bank that wouldn’t bail out Wall Street at the first hint of trouble, banks had a natural aversion to excessively high levels of leverage. However, because of Alan Greenspan (#29) and the “Greenspan put,” banks became far less reticent about using enormous amounts of leverage in the interest of generating the biggest returns. The combination of a completely unregulated market in derivatives with the active central bank of Alan Greenspan dedicated to providing constant succor and support to Wall Street was a disaster waiting to happen. It would prove to be a disaster the world wouldn’t have to wait long for.

Well before the July 1998 hearings on derivatives or even the May 1998 proposal to subject derivative securities to some sort of regulation, financial derivatives had generated considerable scrutiny from within the banking establishment. In a January 1992 speech to the New York Bankers Association Gerald Corrigan, the Governor of the Federal Reserve Bank of New York, cautioned bankers about the danger of financial derivatives. He warned bankers they need to “take a very hard look at off balance sheet activities (derivatives)” and “I hope this sounds like a warning because it is.” Later that year Allan Taylor, Chairman of the Royal Bank of Canada, likened derivatives to a “time bomb that could explode just like the LDC crisis did, threatening the world financial system.” (The LDC crisis was the crisis spawned by hundreds of billions of loans to third world countries going bad.) Picking up on the bomb metaphor, Felix Rohatyn, a senior partner at investment bank Lazard Freres, likened the market for derivatives as “26-year- olds with computers creating financial hydrogen bombs.”

As these concerns show, the post-crisis criticism of Summers and others for failing to act on derivatives in July 1998 is not Monday morning quarterbacking. The dangers inherent in derivatives and the enormous leverage that could be employed with them had been topics of discussion for years, particularly among the more conservative elements of the banking establishment. Given these concerns, what explains the enormous resistance to Born’s seemingly modest proposal that clearly had some merit, and would simply treat derivative investments in the same way that other investments were already being treated? The simple reason is regulating derivatives would - in the opinion of Larry Summers, the biggest banks on Wall Street and the supposedly brightest members of Ivy League economics departments – kill the proverbial goose that laid golden eggs.

Larry Summers and the rest of the economic establishment believed they could marry their economic insights – the most obvious manifestation of which was a raft of completely worthless, nonsensical equations – with the power of modern computers to precisely model not only entire national economies, but small, virtually imperceptible differences between the market price of an asset and its computer predicted “fair” price. Stripped of their mathematical complexity and Ivy League pedigrees, the complicated economic models used in trading derivatives rested on three enormous blunders;

- Prices from the past could be used to predict prices in the future

- The models confused correlation with causation

- People always act rationally

These mistakes are so basic and the ignorance of them so replete with enormous risks, that PhD economists - particularly those, like Summers, with degrees from Harvard or MIT - are about the only “educated” people walking the face of the earth dumb enough to make them.

Armed with their sophisticated mathematical models – which weren’t worth the paper they were written on – hedge funds, investment banks and PhD economists like Larry Summers believed they had created a financial perpetual motion machine. Once started, this machine would effortlessly and continuously generate enormous trading profits. Unlike the voodoo science which modern economics has clearly become and the witch doctor economists who are its chief practitioners, in the rigorous, rule-based field of thermodynamics, engineers recognize that perpetual motion machines can’t exist. They are simply too good to be true. Regrettably, the simple notion of something being too good to be true was lost on the largest Wall Street banks and their financial errand boys in the Treasury Department like Larry Summers.

An understanding of the trade in derivatives and the models used to justify these trades can be gained by using government bonds as an example. Government bonds will yield different rates of interest depending on the country issuing the bonds. For example, German bonds will always pay less interest than an equivalent French bond because Germany has a much better record of diligence, living within its means and keeping its financial wits about itself than France. Based on historical data, statistical regressions of this data and – laughably - assuming a normal distribution to this historical data - it was believed that it was possible to determine if the spread between German and French bonds was too high, too low or optimally priced. If the bonds were mispriced, then a derivative security could be established based on the interest rate spread between the bonds narrowing or widening.

In addition to the complete implausibility of believing historical data would flawless predict prices in the future, another problem with trading derivatives was the very small difference in prices predicted by the model and those prevailing in the market. Returning to the example of government bonds, the difference in the interest payments between German and French bonds – or the “spread” - might only be a small fraction of a percentage point – say 0.25%. Because the spreads were so small, the only way to make serious money on derivative investments of this type was to use enormous leverage.

Long Term Capital Management, LTCM, was the poster child for derivative investments in the 1990s, and a review of their history proves the importance of leverage to a strategy based on derivatives. In 1995, LTCM generated a total return of 59% on its capital. However, its return on total assets – which accounts for the enormous amounts of borrowed money and leverage – was just 2.5%! Basically, LTCM used enormous amounts of borrowed money to enter hundreds of trades each year, and only hoped to make a very small return on each of these trades. While the return on any one trade would be small, the total return on all the trades – the vast majority of which were made with borrowed money – would allow the total return on capital to be enormous. PhD economists like Lawrence Summers considered their models to be so accurate and precise that even with enormous leverage, it was virtually impossible to lose money.

Of course, the confidence the economic establishment had in their models was completely misplaced. Moreover, because of the enormous amounts of leverage used and the relatively small returns that could be gained with any one trade, the strategy used to trade derivatives was the Wall Street equivalent of picking up pennies in front of a runaway freight train; the potential returns were completely dwarfed by the potential losses.

Amazingly, not long after the July 1998 hearings ended, LTCM suffered a spectacular collapse in September. LTCM’s collapse was considered so serious and potentially damaging to the entire financial system that the Federal Reserve Bank of New York organized a Wall Street bailout of LTCM to avoid a financial panic. Most disastrously, the Fed’s Alan Greenspan (#29) essentially duplicated the mistakes made by the Fed’s Ben Strong 71-years earlier. Greenspan didn’t call a secret meeting of the world’s most important central bankers; instead, in October 1998 he cut rates between regularly scheduled meetings of the Fed’s Open Market Committee (FOMC).

In doing so Greenspan gave Wall Street the proverbial greenlight to start a period of virtually unprecedented speculative excess, and Wall Street was more than happy to drop the clutch. From Greenspan’s irresponsible interest rate cut in October 1998 through March 2000, the NASDAQ soared from 1,611 to just over 5,000. However - and duplicating what happens after every speculative bubble - the market fell even faster than it rose. From its peak in March 2000 to its bottom at 1,114 in October 2001, the NASDAQ suffered a nearly 80% drop. Unfortunately, Alan Greenspan and the Fed weren’t finished with interfering in the economy and would cause far more damage.

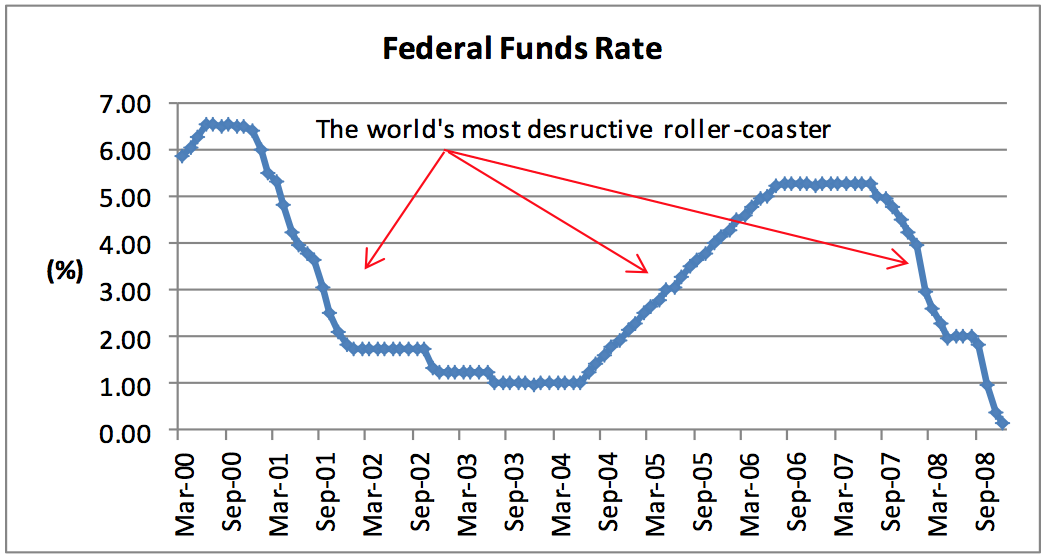

In response to the tech bubble collapse – the climax run of which was fueled by his October 1998 rate cut - Greenspan and his partner in criminal stupidity, Ben Bernanke (#3), would then embark on an enormous interest rate cutting spree. It is important to realize that interest rates just didn’t fall in the early 2000s, they fell off a cliff. See the chart below, data is from the St. Louis Fed;

In the same way an unscrupulous football trainer would shoot up his team’s star running back with high-strength pain killers to mask the pain of a dislocated shoulder, the Federal Reserve slashed rates to deaden the economy to the dislocations caused by the stock bubble collapse. From just March 2000, the top of the NASDAQ bubble, to December 2001 rates fell from 5.85% to just 1.82%. To put the 1.82% rate into perspective, the last time rates were this low for any period of time was during the Eisenhower administration. Rates stayed below the unprecedented low level of 1.25% for years on end! While the Fed’s rate cutting spree did mask some of the short-term economic pain created by the tech bubble collapse, the long-term damage these rate cuts caused was more destructive than any short term pain that was alleviated. The Fed’s rate cutting spree fueled the terminal states of a bubble that dwarfed the recently collapsed bubble in tech stocks – the world altering housing bubble.

Essentially, the derivative inspired failure of LTCM caused the Fed to act irresponsibly, which then fueled even more speculative excess on Wall Street in the form of the tech bubble. When the tech bubble collapsed, the Fed embarked on another round of even more irresponsible policies and this helped to fuel the terminal states of the housing bubble. On this basis alone, it is pretty safe to say that the July 1998 hearings on derivatives and the enormous efforts spent to keep derivatives unregulated had a lot to do with the housing crisis. Thanks Larry!

Even without understanding the chain reaction that started with the collapse of LTCM and ended with the collapse of the housing bubble, it is difficult for any fair-minded person to understand how the failure of LTCM – coming as soon as it did after the July 1998 hearings on derivatives – didn’t prompt the issue of derivatives to be revisited. The fact that even after LTCM collapsed derivatives were left unregulated is clear evidence of the enormous power held by financiers in today’s political environment. The issue of derivatives and their regulation would never be decided on the basis of any sort of objective weighing of merits. Instead, the financial powers to be didn’t want to see derivatives regulated, and this is what they were going to get – no questions asked!

Equally representative of the enormous power held by the financial services industry is the timing of the July 1998 hearings. Note in particular how quickly the hearings were held and who took part in them. Brooksley Born’s proposed her ideas in May and hearings were scheduled for July? That seems pretty fast! In these hearings, President Clinton quickly dispatched his two most senior figures in the Treasury Department, Summers and Robert Rubin (#41), to lead the administration’s efforts to fight – tooth and nail – against Brooksley Born’s proposal. The Fed’s ubiquitous Alan Greenspan (#29) joined the fight as well and was later joined by Arthur Levitt of the Securities and Exchange Commission (SEC).

Brooksley Born led a tiny commission – the Commodity Futures Trading Commission (CFTC) – and the CFTC was no watch for the combined and quickly assembled might of the Clinton administration, the Fed and the SEC. The “Kodak moment” of the July 1998 hearings must be Summers – doing his best impression of an unmade bed – simultaneously slouching and glaring at Born while she calmly and dispassionately – made the case for regulating financial derivatives. Against the enormous bulk that was sloppily and hastily organized against her – personified as it was by the slovenly Lawrence Summers – Born’s proposal never had a chance.

Additional Information:

See Lloyd Blankfein (#4) for more information on the derivative trade in mortgage bond insurance. See Jon Corzine (#13) for more information on the LTCM bailout. For another Harvard educated person who never learned enough to know when he was wrong, see Barney Frank (#21). See Gary Gorton (#27) and Mark Rubinstein (#42) for more information on the highly-leveraged nature of derivative trades and how they can be likened to picking up pennies in front of a freight train. For the disastrous impact of LTCMs collapse on the Federal Reserve, see Alan Greenspan (#29). See Sanford Weil (#48) for another example of how the financial powers that be can quickly prompt their errand boys in government to do their bidding.